Not for Profit entities face unique accounting challenges.

As a result, the Australian Accounting Standards Board (AASB) has historically issued multiple industry-specific standards to support consistent financial reporting across the industry.

Effective for years commencing on or after 1 January 2019, AASB 1058 Income of Not for Profit Entities was established to assist management of Not for Profit entities in recording income where AASB 15 Revenue from Contracts with Customers does not apply. AASB 1058 operates as a partial replacement for the legacy AASB 1004 Contributions that remain current in an amended form.

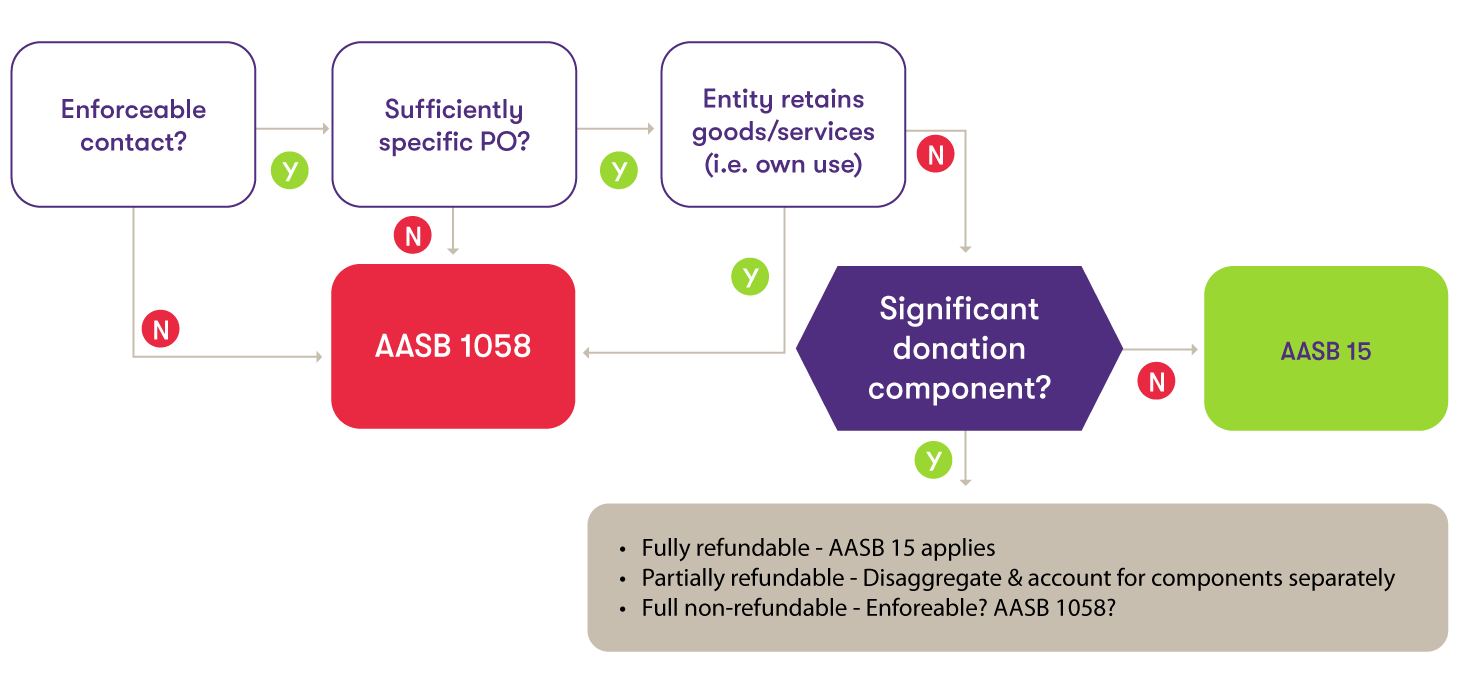

Generally, the appropriate standard, either AASB 1058 or AASB 15, is applied according to a decision tree. Certain entities, particularly government entities, do not have full access to the aforementioned policy choices.![Not for Profit Entities]()

Key impacts – timing of revenue/income

Certain key judgements are required within the decision tree, most especially in determining what is 'sufficiently specific'. Guidance on the topic is included in AASB 1058, however, complexity exists that may give rise to significant differences in the timing of revenue.

For example, consider a case where a payment is received to provide services to the community. If it is determined that the requirements for the rights to that payment are sufficiently specific – for example, the payment requires a certain number of people to be provided services – the revenue is recognised according to the requirements of AASB 15 and it is likely that the revenue will be recognised over time.

If it is determined that the rights to the payment are not sufficiently specific – for example, the only requirement is that it be spent for the betterment of the community – the income is recognised according to AASB 1058 and likely to be recognised as income upon receipt.

Specific guidance is also provided as it relates to contributions received for the explicit purpose of acquiring a non-financial asset. AASB 1058 requires, generally, that revenue be recognised as the entity satisfies its obligations under the acquisition (i.e. upon purchase of a pre-existing asset or on an over-time basis if construction is required).

Key impacts – revenue measurement

AASB 1058 generally requires that benefits received for the purpose of meeting the objectives of a not-for-profit entity be measured at their fair value and income recognised equal to that fair value (for example, donated assets). Certain policy decisions are available for specific topics.

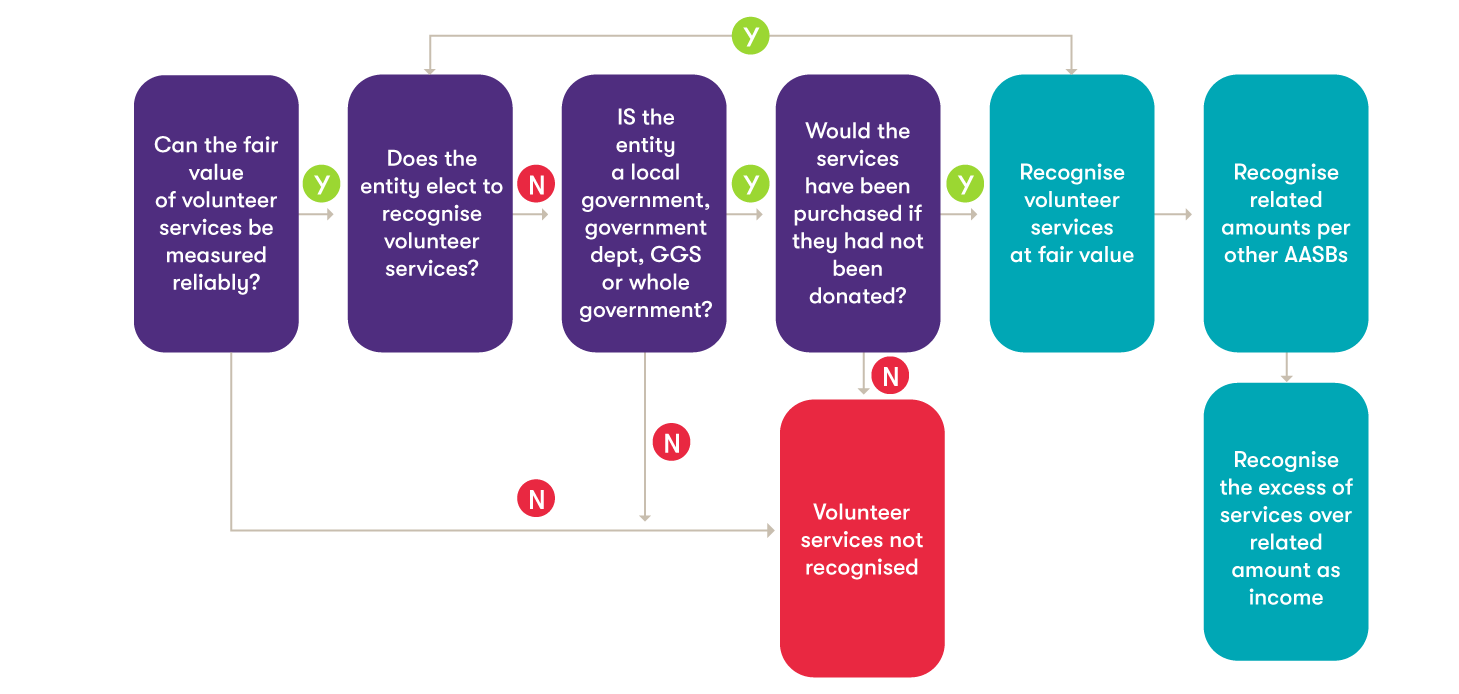

Volunteer services

Volunteer services are able (for non-government entities) to be excluded from recognition or recognised either as an expense (with commensurate revenue) or as an asset (if AASB 116 or AASB 138 applies).

![Not for Profit Entities]()

Peppercorn leases

'Peppercorn' leases are leases entered into for payment significantly below market value. Traditionally, payment was in the form of 'one peppercorn' to enable a legal contract to be established.

AASB 1058, as originally drafted, required that such non-market leases are recorded at market value with the excess benefit received is recognised as income. It was subsequently amended such that entities are able to make a policy election to either record the lease at its market value or at its contract value.

We anticipate that most entities will elect to record at contract value to minimise the cost of implementation and volatility in net income.