Treasury has released draft regulations supporting the Treasury Laws Amendment (Building a Stronger and Fairer Super System) Act 2026, which introduced the new Division 296 tax on earnings attributable to the portion of superannuation balances above thresholds of $3m and $10m.

The regulations provide the long-awaited operational detail on how the new tax will work in practice, particularly for defined benefit interests, large Australian Prudential Regulation Authority (APRA) funds and Self-managed Superannuation Funds (SMSFs).

These draft regulations are currently open for submission until 7 April 2026.

They outline the operation and implementation of the following:

- how Division 296 Earnings are split between members

- calculation of earnings for defined benefit pensions

- super interests that are excluded from Div 296

- how Division 296 applies in the year of, and after death.

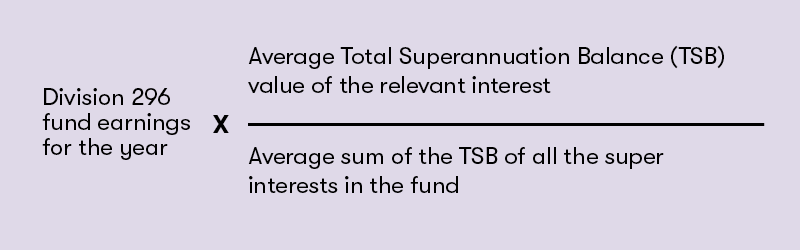

How Division 296 Earnings are split between members

SMSF’s with more than one member will be required to split Division 296 earnings between members via an actuarial certificate. SMSFs with nil Division 296 earnings or no ‘in-scope’ members will not need to obtain an actuarial certificate. The base formula for this calculation is outlined below::

![]()

See below an example of where an SMSF has two members:

If the fund has $500,000 of Division 296 fund earnings, then:

- $300,000 is attributed to Member A

- $200,000 is attributed to Member B.

Only Member A may have a Division 296 tax liability, but the fund must still report both allocations.

Calculation of TSB and earnings for defined benefit pensions

Unlike Account Based, Market Linked and other legacy pensions, Defined Benefit Pensions cannot be measured by actual assets or investment earnings. Instead, it is defined by a person’s entitlement to superannuation benefits by reference to a predetermined income, calculated based on a formula including, length of service and final salary.

Draft regulations outline that Defined benefit pension TSB’s will be determined on an “actuarial valuation method”, like family law valuation methods. Earnings will be subject to the movement between closing and opening TSB, adjusted for contributions and withdrawals, with the final result multiplied by a defined benefit reduction factor. The draft regulations apply a prescribed factor of 0.825 (17.5 per cent reduction) to adjust relevant superannuation earnings

A worked example based on the proposed reduction factor of 17.5 per cent for a pre-retirement benefit:

|

Measure

|

Amount

|

|

TSB start of year – family law value

|

$3.45m

|

|

TSB end of year – family law value

|

$3.60m

|

|

Contributions made for the year

|

$30,000

|

|

Withdrawals made

|

$0

|

|

Total movement

|

$120,000

|

|

Less 17.5%

|

$102,128 Division 296 Earnings

|

|

Percentage of TSB above $3m

|

20%

|

|

Total Division 296 Tax Liability

|

$3,064

|

A worked example based on a reduction factor of 17.5 per cent for a post-retirement benefit:

|

Measure

|

Amount

|

|

TSB start of year – family law value

|

$3.45m

|

|

TSB end of year – family law value

|

$3.60m

|

|

Contributions made for the year

|

$0

|

|

Withdrawals made

|

$280,000

|

|

Total movement

|

$430,000

|

|

Less 17.5%

|

$365,957 Division 296 Earnings

|

|

Percentage of TSB above $3m

|

20%

|

|

Total Division 296 Tax Liability

|

$10,979

|

Super interests excluded from Division 296

The regulations confirm that certain interests are excluded from the Division 296 regime, and are not required to be considered when attributing Division 296 fund earnings, including:

- child pensions sourced from death benefits

- structured settlement contributions

- constitutionally protected funds

- certain judicial and public sector pensions

- foreign superannuation interests and non complying funds.

How Division 296 applies in the year of, and after death

For the first year of operation only (2026-2027), the TSB applicable will be based on the closing balance at 30 June 2027, and if someone dies during the year, they will not be subject to the tax, provided they died on or prior to the last day of the financial year.

This is not the case for subsequent years, outlining that the TSB for Division 296 purposes will be based on the higher of the opening and closing balance. In the year of death, the Division 296 TSB will be the opening balance (1 July), with Division 296 earnings assessed up until all final death benefits are paid out of the fund, or when another person receives the pension income, such as a reversionary pension.

In some instances, paying out final death benefits may take years due to disputes or lumpy illiquid assets; however, it is expected to estimate future Division 296 earnings and include these in the year of death, which may prove difficult to calculate.

If the pension is reversionary, the balance is transferred to the reversionary beneficiary and will then count towards their TSB for Division 296, meaning that there is no Division 296 earnings on the deceased estate in future years.

We’re here to help

Division 296 represents a significant change for individuals with high superannuation balances. It is crucial for individuals to seek tailored advice and plan accordingly to navigate these changes and the implications for their superannuation and wealth strategies. If you’d like to discuss your current superannuation strategy, please reach out to one of our experts today. For more information, please access our hub.

The above information is provided as an information service only and, therefore, does not constitute financial product advice and should not be relied upon as financial product advice. None of the information provided takes into account your personal objectives, financial situation or needs. You must determine whether the information is appropriate in terms of your particular circumstances. For financial product advice that takes account of your particular objectives, financial situation or needs, you should consider seeking financial advice from an Australian Financial Services licensee before making a financial decision in relation to any of the matters discussed.