Financial reporting thresholds for ‘large’ proprietary companies have been doubled following a recent Australian legislative change which is effective for financial years commencing on or after 1 July 2019.

This is a significant financial reporting development as it relieves many growing small and mid-sized Australian businesses from the requirement to prepare and lodge audited financial statements with the Australian Securities and Investments Commission (ASIC).

Based on Government forecasts, approximately one third of proprietary companies who currently lodge audited financial statements with ASIC will no longer have that obligation under the increased financial reporting thresholds.

We welcome these changes as the increased reporting thresholds will help relieve the compliance burden on many growing small and mid-sized businesses in Australia. We note that the Regulations make no changes for ‘grandfathered’ proprietary companies. Accordingly, grandfathered entities that become ‘small’ as a result of the increased thresholds should consider continuing to have an audit in order to maintain their grandfathered status should the business grow and become ‘large’ again in future.

It’s important to note that a significant amount of entities will still be subject to reporting obligations as a result of their banking or stakeholder agreements outside of Corporations Law. These reporting obligations may be ensuring that an audit still takes place.

The Amendments

Following the public consultation process, the Commonwealth Government issued the final amendments in the form of Corporations Amendment (Proprietary Company Thresholds) Regulation 2019. The new requirements are consistent with the proposals in the Exposure Draft issued in late 2018.

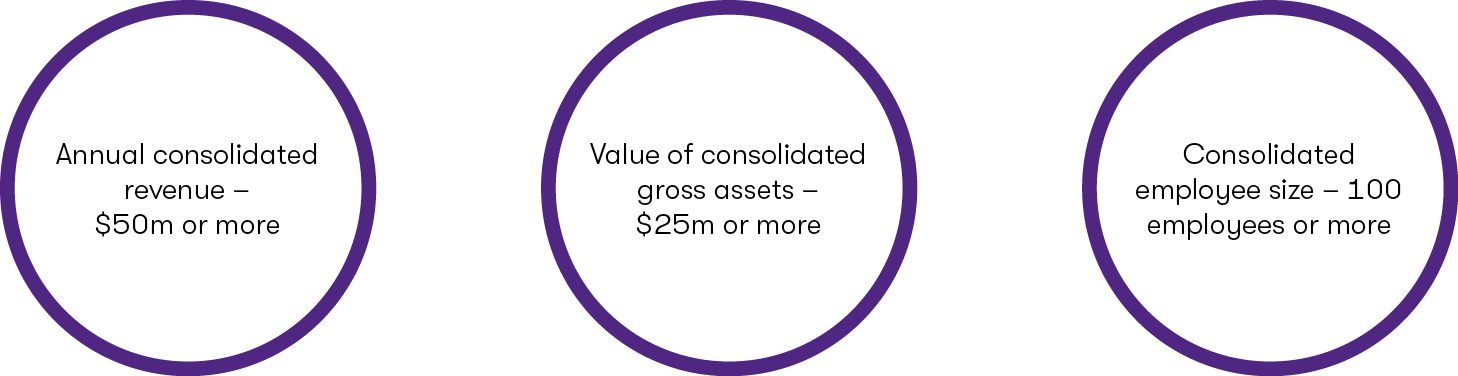

The Regulations adjust the thresholds by doubling them as follows:

![GTAL_2019_PA_alert_Diagram_290519.png]()

The increase in thresholds is intended to ensure financial reporting obligations are targeted at economically significant entities while reducing compliance costs for relatively smaller proprietary companies.

|

What is a large propriety company?

The Corporations Act 2001 requires ‘large’ proprietary companies to lodge audited financial statements with ASIC whereas ‘small’ proprietary companies are only required to lodge audited financial statements if directed by ASIC or where requested by more than five percent of their shareholders.

Currently, based on the thresholds introduced back in 2007, a proprietary company is considered ‘large’ for a financial year if it satisfies at least two of the following:

- The consolidated revenue for the financial year of the company and any entities it controls is $25 million or more;

- The value of the consolidated gross assets at the end of the financial year of the company and the entities it controls is $12.5 million or more; and

- The company and any entities it controls have 50 or more employees at the end of the financial year.

|