As well as grappling with a weakening economy and an unsettled global trading environment, one consistent theme that stands out in Australia is an increased focus on employment tax compliance, with a raft of law changes, audit activity and landmark cases.

Building on the 2018 Black Economy Package, the ATO has invested in strategies to combat non-compliance for employment taxes and is armed with more data than ever - following the unilateral roll out of Single Touch Payroll. In addition, the sharing of information with the Department of Home Affairs, ASIC, the ASX and AUSTRAC is making significant changes to the visibility of expatriate movements and broader employment tax compliance.

The fallout has led to leading high profile non-compliance cases. In 2019 alone, we've seen a major media outlet, a major airline, many retailers and restaurants, a Big 4 bank and a law firm exposed for under-paying their staff or failure to meet employee Superannuation contributions.

The news is not all bad though. Whilst there is a regulatory environment focusing on employment taxes, initiatives such as Single Touch Payroll and the Superannuation amnesty has presented an opportunity to ease administrative burden and take corrective action.

Single Touch Payroll (STP)

STP is a reporting framework whereby employers automatically provide the ATO payroll and superannuation information at the time it is created (i.e. at the time of payment) using standard business reporting software. Whilst not new in 2019, from 30 June 2019, STP became mandatory for all employers.

Specific to foreign employers with expatriates in Australia are:

- Reporting timing concessions for those operating a shadow payroll.

- Extensions to 30 June 2020 for entities who only have a Pay-As-You-Go (PAYG) withholding number (typically overseas entities without a taxable presence in Australia).

Superannuation compliance and amnesty

The proposed amnesty is now before the Senate. When passed, the amnesty will enable employers who unwittingly short-paid superannuation the opportunity to:

- Remove the $20 per employee per quarter administration charge

- Make the payment of superannuation guarantee charge income tax-deductible

- Remove penalties that would normally apply including the imposition of Part 7 Penalties (of up to 200% of the liability).

The amnesty is due to last 6 months from royal assent so employers should act fast to take advantage. As with any amnesty “carrot”, the stick comes with significant penalties after the amnesty period. The penalties for unpaid super after the amnesty period includes jail terms for employers who deliberately avoid complying with the superannuation guarantee law.

As we have seen with many high profile cases, including a Big 4 accounting firm, it is common for foreign employers with expatriates to not realise their requirements in respect to superannuation so now is a prime opportunity to review compliance.

Black economy measures

Despite the name, the measures introduced are bringing businesses who would not consider themselves subject to the black economy, under scrutiny. Some of these changes are:

- Businesses will no longer be able to claim a deduction for payments to their employees, where they have not withheld any amount of PAYG withholding. This could impact expatriates where the correct procedures and structuring are not followed.

- Taxable payments reporting system (TPRS) requiring the reporting of contractors are extended to Security providers, Road freight transport, Computer system design and related services. This is capturing a number of organisations that have recently been establishing their businesses in Australia.

- Common Reporting Standard (foreign bank account information exchange) as lead on from the FATCA Agreement

Main residence removal for foreign residents

Where previously the sale of a person’s ‘home’ was ordinarily exempt from CGT in Australia, these gains may be taxed in full for foreign residents and the changes could result in a significant tax exposure for current and future globally mobile employees, and in turn, their employers where there are tax equalisation policies in place.

The initial perceived impact of these changes has been focused on the restriction of the main resident exemption for foreign resident investors. However, these changes will have the same impact on:

- Australian citizens who go on assignment overseas and sell their properties during a period of foreign residency.

- Inbound assignees who sell their Australian property after returning to their home country.

The measures, which received royal assent on 12 December 2019, apply retrospectively from 9 May 2017. Further details can be found in our client alert.

Residency Tests – the present and the future

Australia has long had complex rules over Residency. This has been highlighted in 2019 in the Full Federal Court decision in Harding v FCT [2019]. In this case, the High Court refused the Commissioner special leave to appeal and found that the taxpayer had a permanent place of abode in Bahrain. The key decisions, that went against the grain of other ATO cases, is that the tax payer was a non-resident:

- Establishing a ‘place of abode’, outside Australia does not refer only to a specific house, flat or other dwelling, rather is refers to a town or country.

- The location of Mr Harding’s family (who remained in Australia) is not necessarily determinative of an individual’s tax residency.

Changes in the future

In 2019 Treasury undertook a consultation on changes to the current Australian tax residency rules. The proposal contains;

I. primary 'bright-line test' - this test will consider the time spent in Australia (i.e. ‘day count’) to automatically determine the residency status of the majority of individuals; and

II. A secondary test – known as the 'factor test'. Under this test, and for each “factor” an individual satisfies, they can be considered to have a higher level of connection to Australia. This includes factors such as, time spent in Australia; immigration status; family location; accommodation; and economic ties.

We expect continued development and updates on these proposed changes in 2020. Employers of expatriates should be aware of these changes so they are prepared for current and future assignments.

Other news

The Australian/Israel Double Tax Agreement received royal assent on 28 November and the Australia-Hong Kong Free Trade Agreement will enter into force on 17 January 2020.

What should clients be doing

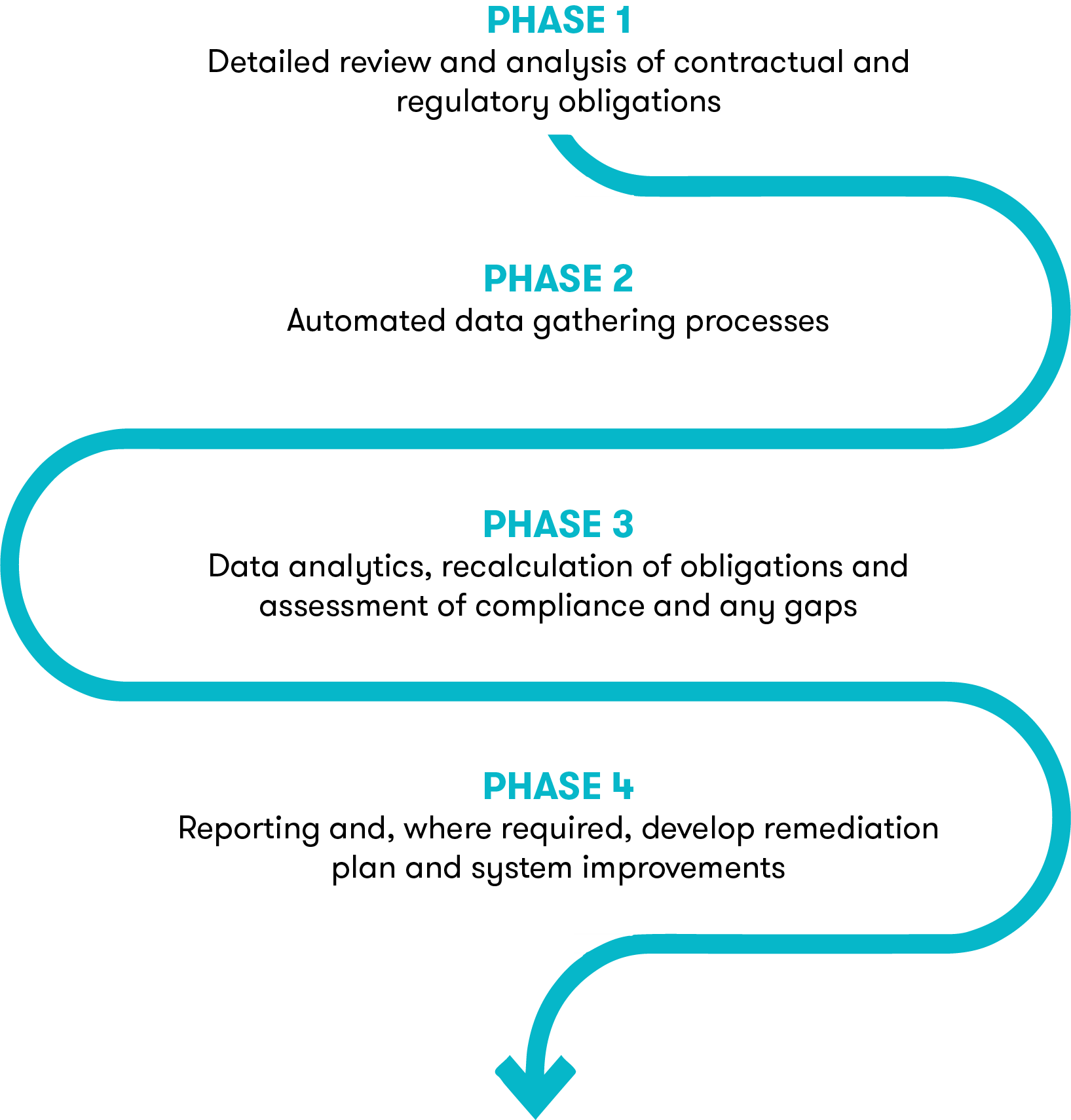

As detailed by these measures, payroll and superannuation have a high-risk profile. This is inherently more complex for expatriates where they may be in receipt of additional benefits and sit outside a businesses core payroll platform or process.

Using our comprehensive Payroll Assurance Review and Recalculation tool, our team applies a lens to the remuneration processes and obligations to identify issues and assist with updating processes for future payments, recalculating correct past amounts, and developing a remediation process where required. Read more.

Payroll Assurance Review and Recalculation process for a robust solution:

![GTAL_2019_GTC_payroll_infographic.png]()