Before taking a well-deserved break over the coming weeks, builders undertaking projects in Queensland should ensure that they are compliant with two significant regulatory obligations that fall due over the New Year period:

1. The roll-out of the Project Trust Account regime to commercial projects; and

2. Annual Financial Reporting to QBCC demonstrating compliance with the Minimum Financial Requirements.

Project Trust Accounts (PTA’s)

The new Trust Account requirements will be phased in gradually, and eligibility for each phase will be defined by who is the project owner (or principal), the contract price for the project, and whether there are subcontractors engaged as follows:

|

Requirement

|

New Commencement Date

|

Previously advised

|

|

New government and hospital and health service contracts > $1m

|

1 July 2021

|

1 July 2020

|

|

Private sector, government owned corporations & local government contracts > $10m

|

1 January 2022

|

1 July 2021

|

|

Private sector, government owned corporations & local government contracts $3m to $10m

|

1 July 2022

|

1 Jan 2022

|

|

Private sector contracts > $1m

|

1 January 2023

|

1 July 2022

|

Those impacted by PTAs should prepare their business for the new layer of administration required for projects and restricted access to cash after the relevant commencement date.

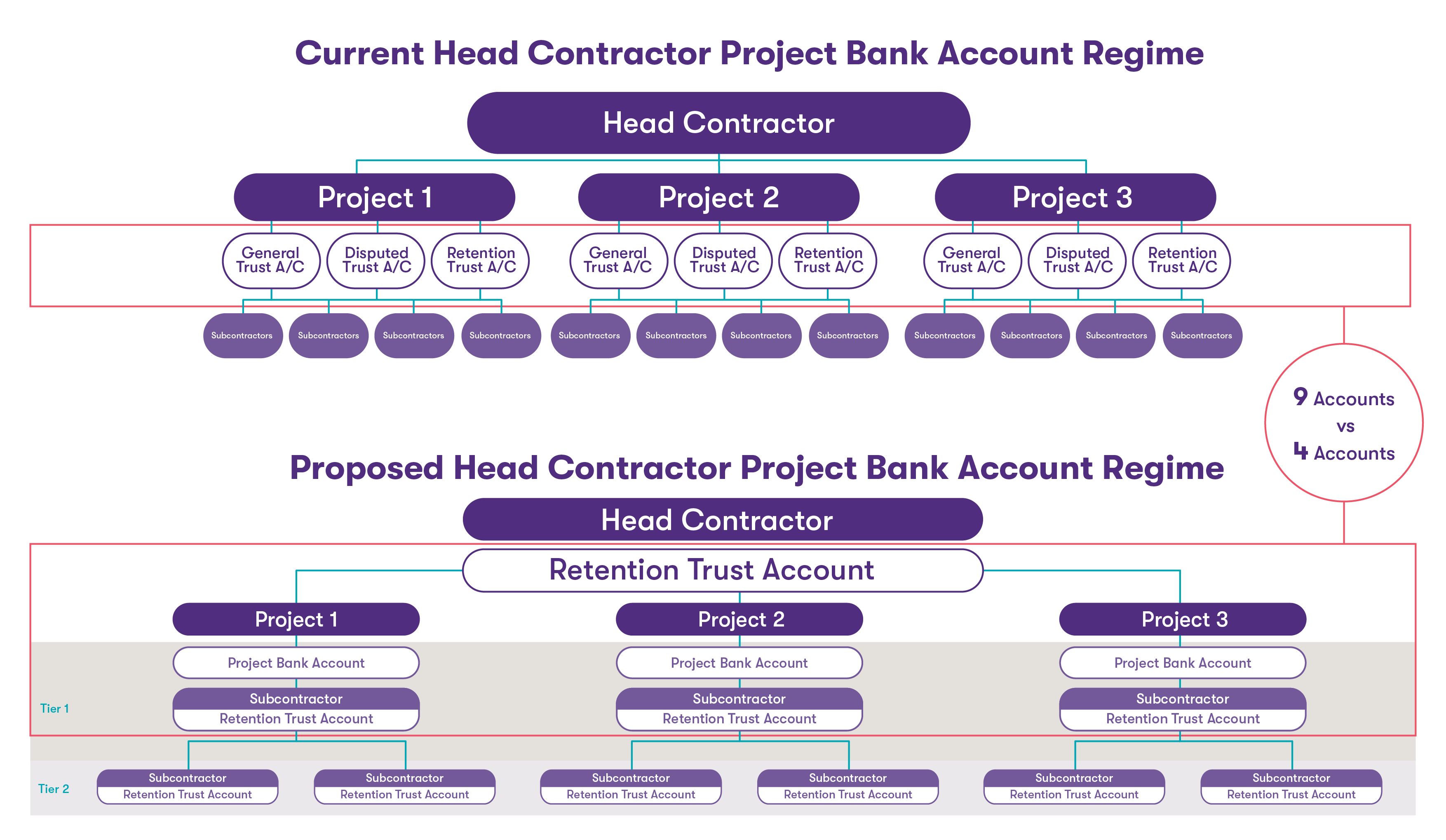

As noted in our previous alerts, the revised PTA roll-out implemented the majority of recommendations made by the Building Industry Fairness Reforms Implementation and Evaluation Panel including the following key changes to the former PBA regime:

- replaced “Project Bank Accounts” with “Project Trust Accounts”

- introduced an obligation to maintain a single Retention Trust Account to manage retention monies

- removed the requirement for a disputed funds trust account

- removal of the requirement for principals to have viewing access of the trust accounts

While head-contractors may be relieved by the simplification of the regime (removal of the requirement to maintain disputed funds trust accounts and retention monies trust accounts on each and every qualifying project), the obligation to maintain a retention trust account will extend to:

- Principals who have engaged a head contractor to carry out project trust work (from 1 January 2022); and

- Subcontractors downstream from a project trust contract who is withholding cash retentions from any of their subcontractors.

![GTAL_2020_REC_Current_PBA_Regime.png]() Click to enlarge

Click to enlarge

Despite the simplification of the regime, head contractors will still incur a significant level of additional administration in managing the new accounts. More information is available from the following QBCC guides:

Minimum Financial Requirements

While most audited builders will have already lodged their audited financial reports for FY21 with the QBCC, builders not subject to external audit have until 31 December 2021 to submit their annual suite of financial information to the QBCC. The following is required to be lodged:

- a profit and loss statement;

- a balance sheet;

- a debtors and creditors report;

- a statement of cashflows;

- notes to the financial statements containing notes required by the Australian Accounting Standards*;

- a written declaration verifying the information contained in the documents mentioned above*; and

- a description of the measurement, within the meaning of the Australian Accounting Standards, on which the financial statements mentioned above, are based and the accounting policies or reports relevant to those financial statements*.

Licencees need to recognise the importance of getting their reporting right and ensuring their balance sheet and structure is meeting the stated requirements.

Failure to meet the QBCC reporting requirements can result in the suspension of a building license and fines of more than $2,600 for individuals and more than $13,000 for companies, or prosecutions for those that do not submit their reports by the due date. There is a long list of examples over recent years where the QBCC has used its power and suspended builders’ licence.

All builders undertaking projects in Queensland should plan ahead to ensure all financial information lodged demonstrates compliance with the Minimum Financial Requirements, and is done so by the deadline.