INTRODUCTION

The purpose of this alert is to draw attention to the release of AASB S2025-1 Amendments to Greenhouse Gas Emissions Disclosures, issued by the Australian Accounting Standards Board (AASB) to amend AASB S2 Climate-related Disclosures (AASB S2).

What are the amendments to AASB S2?

On 17 December 2025, the AASB issued AASB S2025-1 Amendments to Greenhouse Gas Emissions Disclosures to amend AASB S2 to provide additional relief and clarify existing relief relating to specific GHG emissions disclosure requirements, while also meeting the material information needs of users. The amendments are consistent with the Amendments to IFRS S2 Climate-related Disclosures, issued on 11 December 2025 by the International Sustainability Standards Board (ISSB).

What are the implications for AASB S2 reporting entities?

| Topic |

AASB S2 has been amended to: |

Implications for reporting entities: |

Amendment 1 – Scope 3 Category 15 Investments

|

Clarify that an entity is permitted to limit its measurement and disclosure of Scope 3 GHG emissions for Category 15 Investments to financed emissions - those emissions attributable to ‘loans and investments’ made by the entity to investees or counterparties (AASB S2, Appendix A).

|

Current requirement

AASB S2.29(a)(vi)(1) requires that an entity consider all 15 Categories of scope 3 GHG emissions as described in the Corporate Value Chain (Scope 3) Accounting and Reporting Standard when measuring the absolute gross GHG emissions generated during the reporting period.

AASB S2.29(a)(vi)(2) requires that an entity disclose additional information about Category 15 GHG emissions or those associated with its investments (or financed emissions), if the entity’s activities include asset management, commercial banking or insurance.

Amendment

This amendment clarifies that, for Category 15, an entity is only required to measure and disclose GHG emissions arising from financed emissions (i.e. those emissions attributable to ‘loans and investments’ made by the entity to investees or counterparties).

This includes loans, project finance, bonds, equity investments and undrawn loan commitments, and for an entity participating in asset management activities, emissions attributed to assets under management.

The entity is permitted to exclude from its measurement and disclosure of Category 15 GHG emissions the emissions associated with other financial activities, such as facilitated emissions associated with investment banking activities and emissions associated with insurance and reinsurance underwriting activities.

The amendment explicitly excludes emissions associated with derivatives.

|

|

Amendment 2 – Industry classification of financed emissions

|

Permit use of alternative industry classification systems to disaggregate information about financed emissions.

|

Current requirement

AASB S2.B62-63 requires that an entity involved in commercial banking or insurance activities disclose disaggregated information about their financed emissions for each industry by asset class.

The original AASB S2 requirement prescribed the use of the Global Industry Classification Standard (GICS).

Amendment

This amendment permits an entity to use an industry classification system other than GICS to disaggregate emissions for each industry, and to select an industry classification system that enables users to understand the entity’s exposure to climate-related transition risks. For example, Australian entities may prefer to use Australian and New Zealand Standard Industrial Classification (ANZSIC).

Where an entity participates in both commercial banking and insurance activities, it is not required to use the same industry classification system for both activities, but is required to disclose the system used and how the choice assists in understanding the entity’s exposure to climate-related transition risks.

This provides more flexibility when choosing an industry classification system, reducing the potential for duplicative reporting and additional costs where an alternative industry classification system (or entity-specific system) better reflects an entity’s actual exposure to climate-related transition risks.

|

|

Amendment 3 – Jurisdictional relief from using the GHG Protocol: A Corporate Accounting and Reporting Standard (2004)

|

Clarify that jurisdictional relief applies only to the part of the entity that is subject to a jurisdiction-specific requirement to measure emissions using a method other than the GHG Protocol: A Corporate Accounting and Reporting Standard (2004).

|

Current requirement

AASB S2 requires that an entity measure its absolute gross GHG emissions using the GHG Protocol: A Corporate Accounting and Reporting Standard (2004) unless a jurisdictional authority or exchange on which the entity is listed requires measurement using a different approach. This is referred to as ‘jurisdictional relief’.

Amendment

This amendment clarifies that the jurisdictional relief is only applicable to the part of the entity that is subject to that requirement. The parts of an entity that are not subject to that requirement cannot apply the jurisdictional relief.

For example, in Australia, the National Greenhouse and Energy Reporting (NGER) Scheme requires certain entities, by law, to use the National Greenhouse and Energy Reporting (Measurement) Determination (2008) to measure certain scope 1 and 2 GHG emissions. Entities reporting under the NGER Scheme have the option to apply this jurisdictional relief.

Jurisdictional relief is not intended to provide relief from the measurement and disclosure of any GHG emissions that are not required to be measured by a specific jurisdictional method. Such emissions must be measured using the GHG Protocol: A Corporate Accounting and Reporting Standard (2004) instead.

For example, not all GHG emissions are required to be measured in the NGER Scheme, including certain sources of Scope 1 emissions, certain Scope 1 emissions below specific thresholds, and Scope 3 emissions. An entity applying AASB S2 would be required to measure such GHG emissions using the GHG Protocol: A Corporate Accounting and Reporting Standard (2004).

|

|

Amendment 4 – Jurisdictional relief from using global warming potential (GWP) values from the latest IPCC Assessment Report

|

Extends jurisdictional relief to the GWP values used for converting GHG emissions into carbon dioxide equivalent (CO2-e).

|

Current requirement

AASB S2 requires that, where an entity uses direct measurement or an emissions factor that does not convert the underlying emissions into CO2-e, the entity converts the seven constituent GHG[1] using the GWP values based on a 100-year time horizon from the latest IPCC assessment available at the reporting date (currently the Sixth Assessment Report (AR6)). Previously, this was required even if the entity was applying a jurisdictional relief that used a different source of GWP values.

Amendment

This amendment extends the jurisdictional relief to the GWP values, so that an entity, or part of an entity, that is applying the jurisdictional relief in the measurement of GHG emissions is also able to apply the GWP values required by that jurisdictional requirement.

For example, in Australia, the NGER Measurement Determination requires reporters to use the GWP values from the IPCC’s Fifth Assessment Report (AR5). This amendment enables entities that measure certain scope 1 and 2 GHG emissions under the requirements of the NGER Scheme to avoid recalculating those GHG emissions using the GWP values from AR6.

Jurisdictional relief is not intended to provide relief from the measurement and disclosure of any GHG emissions that are not required to be measured by the jurisdictional method. Such emissions must be measured using the GWP values from the latest IPCC assessment available at the reporting date (currently AR6).

For example, not all GHG emissions are required to be measured in the NGER Scheme, including certain sources of Scope 1 emissions, certain Scope 1 emissions below specific thresholds, and Scope 3 emissions. An entity applying AASB S2 would be required to convert the emissions using GWP values from AR6 when using direct measurement or an emissions factor that does not convert the underlying emissions into CO 2-e.

|

Practical application of the amendments to AASB S2 - Examples

Example: Amendment 1 – Commercial bank

Company A is a commercial bank that provides banking services, financial advisory services, and loans to residential and business customers.

Prior to the amendments to AASB S2, Company A had begun to calculate its scope 3 GHG emissions for Category 15 including facilitated emissions attributable to its financial advisory services.

Following the amendments to AASB S2, Company A is permitted to narrow the scope of its Category 15 emissions to only those attributable to its loans and investments.

Example: Amendment 2 – Insurance company

Company B is an insurance company that provides home and contents insurance, motor vehicle insurance, and health insurance.

Prior to the amendments to AASB S2, Company B was required to use the Global Industry Classification Standard (GICS) to disaggregate its financed emissions when disaggregating by industry and asset class.

Following the amendments to AASB S2, Company B is permitted to disaggregate its financed emissions using its existing industry classification system, the Australian and New Zealand Standard Industrial Classification (ANZSIC).

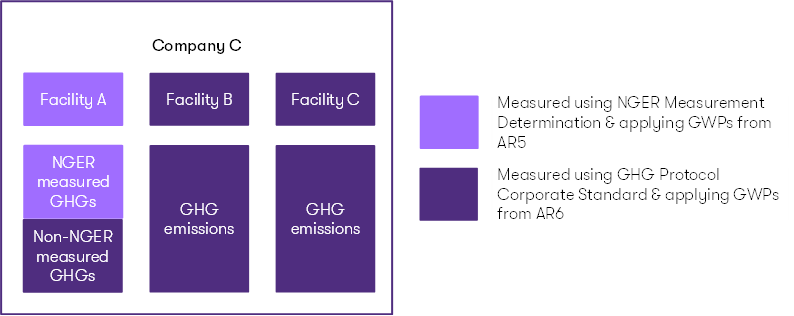

Example: Amendments 3 & 4 – NGER Scheme reporter

Company C has a single facility (Facility A) that is legally required to report certain scope 1 and scope 2 GHG emissions to the Clean Energy Regulator (CER) in compliance with the National Energy and Greenhouse Reporting (NGER) Act (2007). Company C has two other facilities that are not within the scope of the NGER Scheme and are not required to report to the CER (Facility B and Facility C).

Prior to the amendments to AASB S2, Company C was required to recalculate its GHG emissions using the GWP values from the IPCC’s Sixth Assessment Report (AR6). Company C was also uncertain whether it could use its existing NGER measured emissions data for AASB S2 reporting, as it only related to one of the three facilities in Company C, which did not constitute the whole of the reporting entity.

Following the amendments to AASB S2, Company C is able to elect to apply the jurisdictional relief to the single facility’s NGER measured emissions, including using GWP values from the AR5 as required by the NGER Measurement Determination.

For any other facilities or sources of emissions not required to be measured by the NGER Scheme, Company C must measure these emissions using the GHG Protocol, and (where using direct measurement or an emissions factor that does not convert the underlying emissions into CO2-e) converting the seven constituent GHGs using GWP values from AR6.

![]()

AASB FAQs

To support reporting entities with understanding the amendments to AASB S2, the AASB has released Frequently Asked Questions (FAQs) which you may wish to refer to for further clarification.

The AASB together with CSIRO, has also released an explanation of differences between AASB S2 and the NGER Scheme, available here.

When do the amendments apply?

The effective date for the amendments is for annual reporting periods beginning on or after 1 January 2027.

Early adoption of the amendments is permitted but not required. Entities wishing to early adopt the amendments must:

- make the election to early adopt in writing (see the Corporations Act 2001 s336A); and

- disclose the early adoption of the amendments in their Sustainability Report (see Appendix C1B in AASB S2025-1).

For example, the following Director’s minutes may be used for Corporations Act entities:

“In accordance with s336A of the Corporations Act, the Directors are early adopting AASB S2025-1 Amendments to Greenhouse Gas Emissions Disclosures.”

Should we early adopt the amendments?

Entities with financed emissions may wish to early adopt for the following reasons:

- early adoption may narrow the scope of an entity’s Scope 3 Category 15 GHG emissions;

- early adoption removes the requirement to use GICS, with alternatives (such as ANZSIC) permitted; and

- early adoption may support consistent GHG emissions measurement and disclosure across reports, reducing the potential for comparative restatement if only adopted from 1 January 2027.

NGER Scheme reporters may wish to early adopt for the following reasons:

- early adoption enables continued measurement of emissions using the NGER (Measurement) Determination (2008) for relevant part(s) of the entity;

- early adoption removes the need to recalculate NGER emissions using different GWP values; and

- early adoption may support consistent GHG emissions measurement and disclosure, reducing the potential for comparative restatement if only adopted from 1 January 2027.

HOW WE CAN HELP

Grant Thornton has a team of sustainability reporting specialists who understand the intricacies of the AASB S2 requirements and can work closely with you to navigate through the process of getting ready for reporting.

FURTHER INFORMATION

If you wish to discuss any of the information included in this Sustainability Reporting Alert, please get in touch with your local Grant Thornton Australia contact or a member of the Sustainability Reporting Advisory team at sustainability.reporting@au.gt.com.

[1] AASB S2.A[10] defines “greenhouse gases” as “the seven constituent greenhouse gases listed in the Kyoto Protocol – carbon dioxide (CO₂); methane (CH₄); nitrous oxide (N₂O); hydrofluorocarbons (HFCs); nitrogen trifluoride (NF3); perfluorocarbons (PFCs) and sulphur hexafluoride (SF₆).