The current landscape

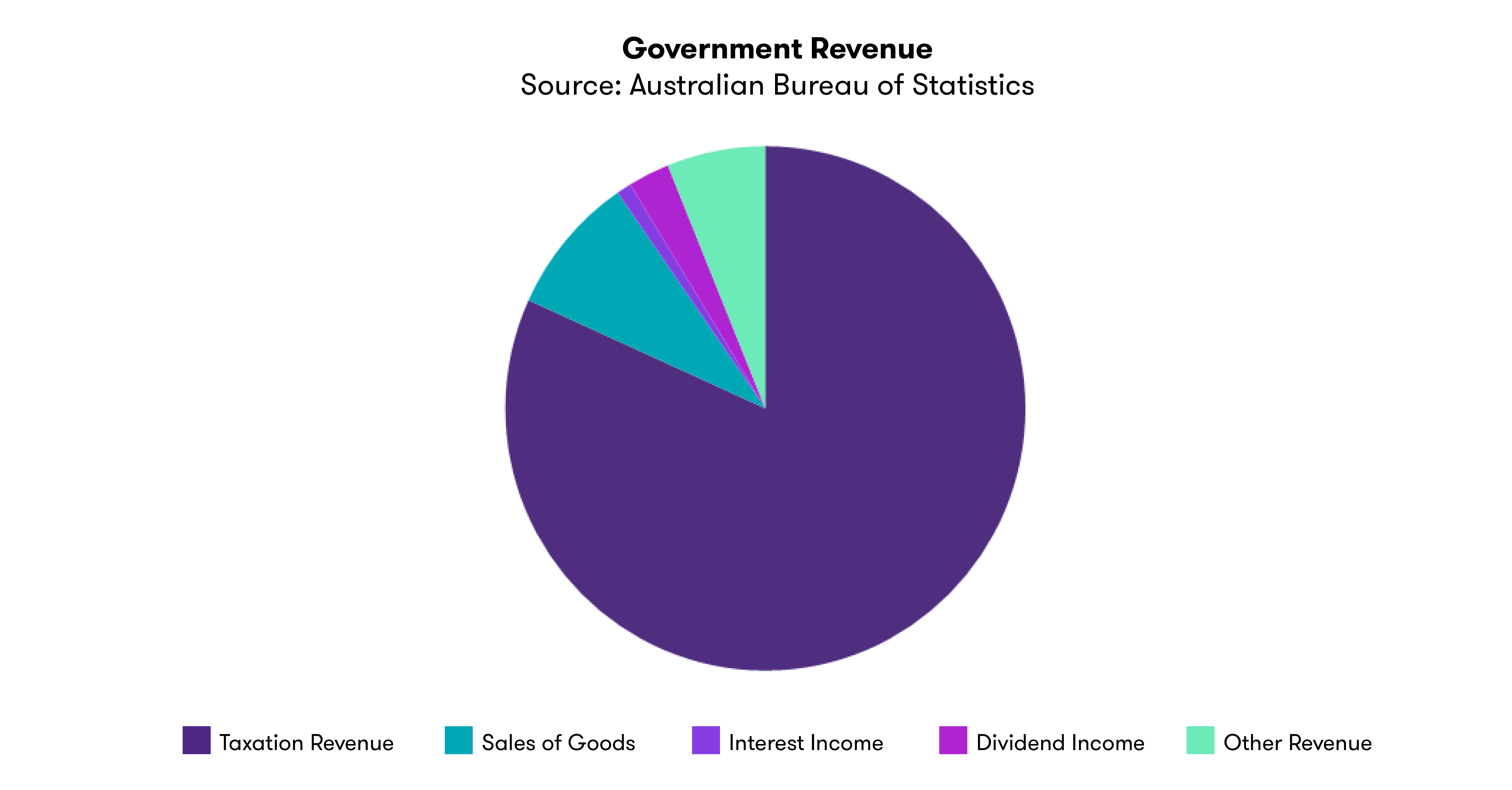

The Federal and State Government’s COVID-19 stimulus measures have resulted in historically unmatched expenditure. With taxes accounting for over 80% of the Government’s revenue, it’s no surprise that we are seeing record high ATO activity.

![GTAL_2022_ATOSeason_Graph1.png]()

![GTAL_2022_ATOSeason_Graph2.png]()

ATO review programs

The ATO has become more structured in administering its corporate taxpayer review programs. Specific programs are in place for public, private and international businesses. Unlike many of the prior ATO review programs, these newer programs target companies and groups based on turnover, with all companies/groups within prescribed turnover parameters to be reviewed. There no longer any “falling through the cracks” situations.

My focus has been on public and international businesses, principally under the Top 1000 Streamline Tax Assurance Review program. This programs targets listed and international businesses that turnover more than $250M, however as the program is nearing completion the ATO have advised that they will be progressing onto lower turnover businesses.

What learnings can we take from the ATO reviews to date

The ATO programs are to be viewed as reviews and not audits. Although there are reoccurring areas of specific ATO focus (such as transfer pricing, tax loss availability, tax consolidations and tax treatment of major transactions/restructures), the primary focus of the review is on the broader tax framework the business operates under.

Specifically, the ATO determines whether a tax framework exists that allows businesses to identify and appropriately adhere to it tax obligations, and can appropriately substantiate this through documented support.

The intent of the reviews is to provide the ATO with “justified trust” that a business has a framework in place that ensures it has paid, and will pay, the appropriate amount of tax.

How to be prepared

Businesses must ensure that an appropriate tax governance framework exists. The ATO will tailor their expectations of the detail and formality of the tax governance framework to the size and complexity of the business.

A functioning tax framework should be demonstrate some of the following:

- specialist tax input for more complicated matters (whether it be an internal or external resource) such as significant transactions or restructures;

- clear and documented communication between a businesses’ Management and its Board regarding critical tax matters and risk;

- an understanding of the ATO’s published areas of concern; and

- documented substantiation of tax positions taken for major transactions/event and in the completion of tax returns.

We have considerable experience in assisting businesses be ATO review ready, in establishing a documented tax governance framework and guiding them through the review process and are here to help.

Learn more about how our Tax services can help you