In our last article, we observed how the developed world’s common pandemic experience of cheap borrowing costs, unprecedented government economic stimulus, and the diversion of services/experience spending had resulted in a surge in demand for real estate across the globe, resulting in the highest levels of material and labour cost inflation experienced in the building and construction industry for many decades.

In our second instalment in this series, we explore time delays – a complementary issue to this unprecedented convergence of surging demand and restricted supply chains. Time can be a killer in business, none more so than for builders burning overhead and facing delay claims on wafer thin project margins.

Production shortages

Anecdotal reports suggest supplier lead times have blown out across all manner of materials including:

| Concrete Slabs |

1 week now 3 weeks |

| Concrete Pipe |

6 weeks now 30 weeks |

| Frames and Trusses |

3 weeks now 13 weeks |

Mathematics dictates that in a world where production of a particular product is constant and inventory is managed on a ‘just in time” basis, if demand for that product doubles, buyers may then have to wait twice as long for its delivery.

Are we currently experiencing a surge in demand combined with restricted supply? It seems so.

Timber Products

Structural Pine has received a good deal of press in recent months for being in short supply. Before COVID-19, the most significant economic event facing Australia was the 2020 bushfire disaster. While the Australian Forest Products Association represents 18 million hectares, it’s estimated that 50,000 hectares (or roughly 40%) of the softwood plantation area in the South West Slopes and Bombala regions of NSW were ravaged by bushfires that season. Over 6,000 hectares of plantations in northeast Victoria were also subject to fire damage, while approximately 95% of privately owned plantations on Kangaroo Island in South Australia were adversely affected. However, Australia was not alone in this issue, with California and Europe also experiencing large losses of commercial forestry reserves to wildfire across 2019-2020.

Builders are still at risk that suppliers, facing their own supply-chain issues, may fail to deliver the full ordered quantity on the scheduled time.

One local truss supplier confirmed that delivery times for raw materials can’t be predicted and suppliers have been pushing out agreed delivery dates. This is forcing them to order whatever stock they can get hold of from the suppliers, but still their facility is operating at only 75% capacity of what they could be producing.

Reductions in Chinese steel production

While the majority of Australia’s steel is sourced domestically (Infrabuild and Bluescope), domestic producers alone have struggled to satisfy the current surge in demand. Bluescope Steel’s production volumes had already increased 15% in the year ended 30 June 2021.

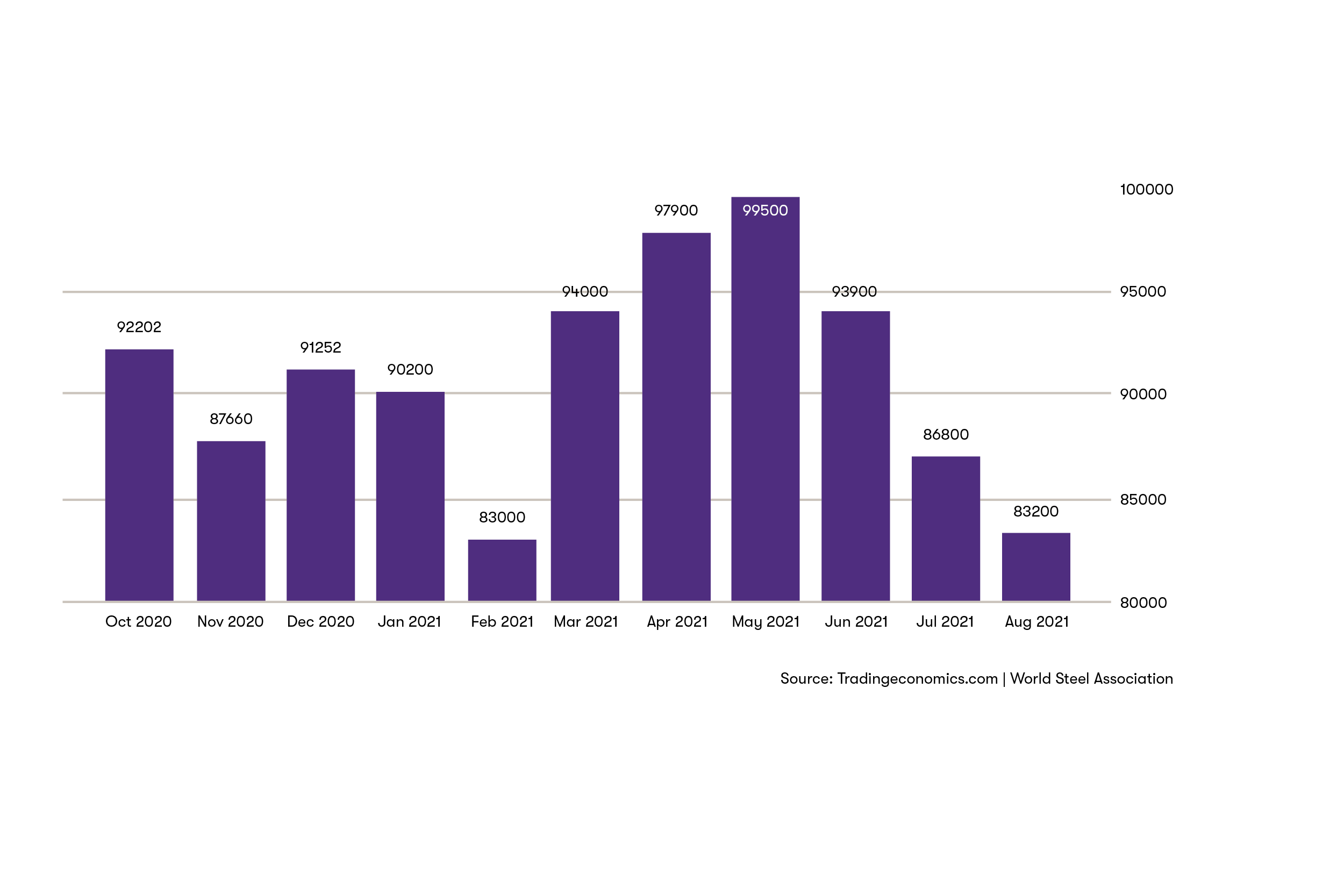

Roughly 30% of Australia’s steel is sourced from China, and in an attempt to reduce carbon emissions, China has announced it will restrict the production of crude steel. With a reduction of almost 20% to date (from almost 100,000 kilotonnes in May 2021 to 83,200 kilotonnes produced in August 2021) - expectations are that in the short term at least, Beijing will continue to wind-back production to improve air quality for the Beijing Winter Games in February 2022.

![Graph_1.png]()

China’s zero tolerance approach to managing the pandemic has also meant that recent outbreaks of the Delta strain continue to interrupt the operation of production facilities and mainland logistics networks.

While Rebar (short for reinforcing bar) prices have stabilised since peaking in May 2021, continued interruptions in Chinese supply could result in further price hikes if we assume global demand is at least sustained. On a positive note, the emerging ‘Evergrande’ problem in the Chinese Real Estate and Construction market suggests that the competition from mainland Chinese builders for steel over coming years could be subdued relative to recent years.

Delays in shipping

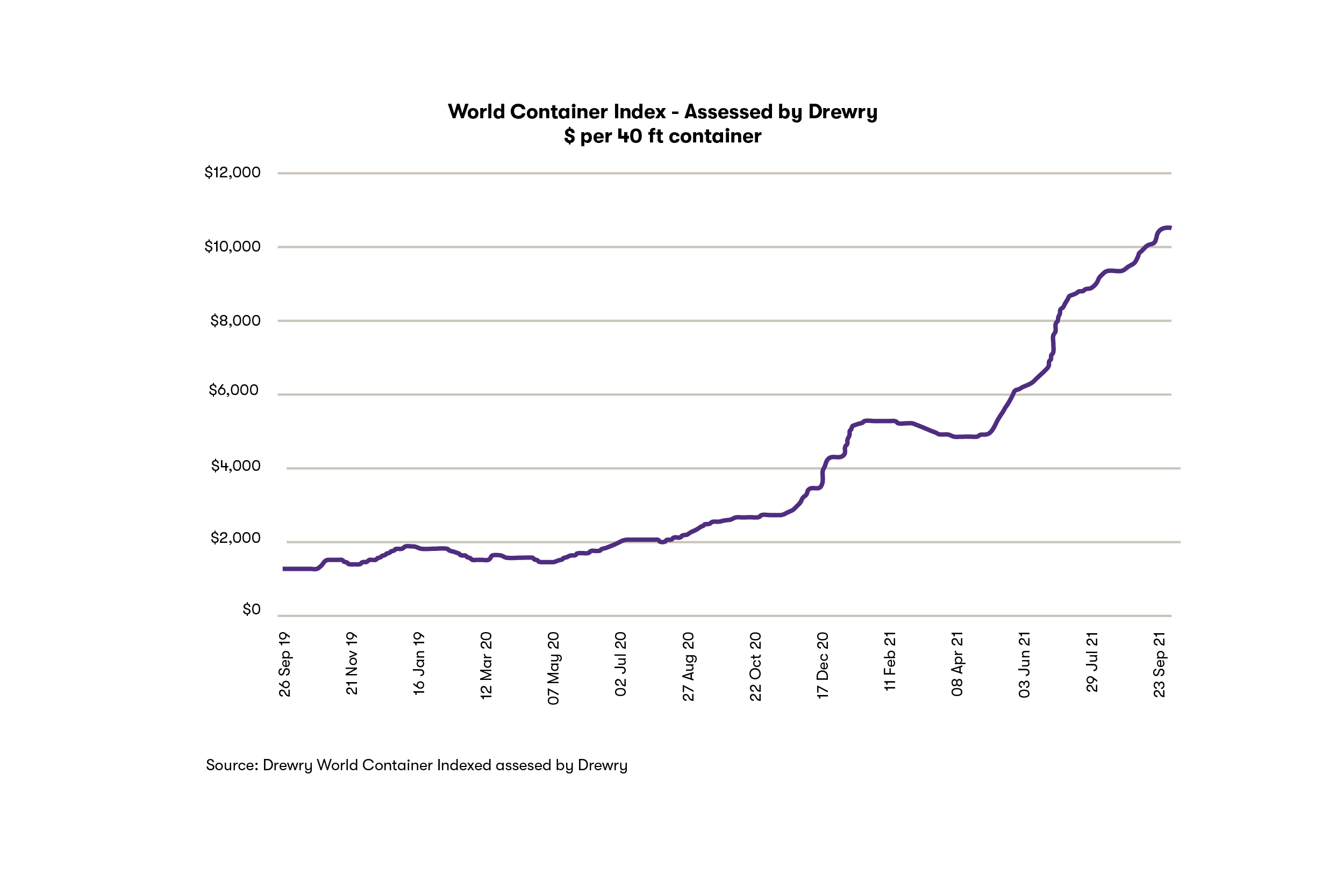

According to Freightos (an online digital booking platform), on 5 October 2021, the cost of shipping a 40 foot container from Shanghai to Sydney on the spot market was over A$11,000. Research consultancy firm Drewry report that the average cost of shipping a standard large (40ft) container is four times greater than it was a year ago, with the average door-to-door shipping time for ocean freight increasing from 41 days to 70 days.

![Graph_2.png]()

Container ships move roughly 25% of the globe’s traded goods by volume. In response to the COVID-19 pandemic, shipping firms expecting a collapse in trade had idled 11% of the global fleet. However, consumer economies (including Australia and America), flush with cash, started spending and trade levels held.

In the first half of 2021, cargo volumes between Asia and North America were up 27% compared with pre-pandemic levels, according to the leading shipping owners association, BIMCO.

In this period of high demand and restricted supplies, pressure is on the shipping industry to move more goods. When new ship builds to increase capacity require a 2-3 year wait, they have limited opportunity to respond quickly - hence the prices rise while demand remains high.

It’s not only the vessels to run the routes, but the limited supply of containers that is causing the delays and both are contributing to the shortage of building material imports. The bulkier the goods, the greater the impact of higher shipping costs. Kwame Asumadu, director of Victorian-based importer WoodPanels Australia, recently wrote to Liberal MP Tim Wilson, chairman of the standing committee on economics, stating the costs of shipping a 40-foot container from New Zealand to Australia had risen by thousands of dollars over the past six months and that shipping lines appeared to be rationing space, contributing to the shortage of building materials in Australia.

The worst may yet be to come, with suggestions that up to 60% of goods to this point were covered under pre-fixed shipping rates and only the balance exposed to soaring spot prices.

Retailers will also be scrambling to stock the shelves as we head into Christmas, which has prompted “peak season” surcharges for all cargo from many Asian ports to Australia. Australian builders will be vying for space and paying a premium to get hold of imported materials through the pre-Christmas rush.

Even once the goods arrive, delays have been encountered at ports in Sydney and Melbourne, which have suffered temporary closures because of workers testing positive to coronavirus.

Where to from here?

According to the Australian Steel Association, import prices have almost doubled over the past year for structural steel products. However the chief concern for many builders right now is not the extra cost of steel, but how the delayed supply is impacting their delivery obligations and resourcing costs.

To this end, reliability is now the key decision driver when choosing suppliers. What was previously a global trend of “just in time” inventory management has now been replaced with “just in case”, and an increased willingness (where possible) to buy locally even at a premium?

Demand for building products remains strong and experts expect it may be at least 6-12 months before the current surge in global demand begins working its way through the supply chain bottlenecks.

In the meantime, labour shortages and government restrictions on on-site staffing present further delay risks on projects.

Key Parties at risk

Again, the extent of delays experienced by builders in the delivery of materials will vary between operators. Larger established operators will likely hold sufficient purchasing power and relationships to get to the front of the queue for materials as they become available. Smaller operators by comparison may be more exposed with minimal material purchasing power.

Anecdotal feedback from industry participants suggests that the average build period for detached dwellings has increased from seven months pre-pandemic to the current timing of up to eleven months. Assuming that workers cannot be readily deployed onto other productive projects during wait periods, this could translate to a reduction in monthly turnover of greater than 30%. The risk of material delays when combined with the cost pressures detailed in our previous article, hardly make for ideal business conditions.

Builders who contracted ambitiously on terms and price to secure pipeline revenue in late 2020 and early 2021 – a time when the most significant supply chain constraints hadn’t manifested – are most at risk of incurring significant losses as a result of delays and cost blow-outs occurring while delivering these projects in the current cycle.

Recommendations

Additional lead times need not result in project delays if project delivery plans order key materials sufficiently in advance. Notwithstanding this, the current environment presents an elevated risk of eating into preliminaries at the front end of contracts, and delay claims at the back end.

While the apparent solution is for builders to avoid contracts that leave them exposed to punitive or liquidated damages resulting from delays, their inclusion in contracts is more often than not the norm demanded by developers and financiers alike. Where a ‘cost-plus’ or ‘schedule of rates’ arrangement is off the table, builders should ensure that either project milestones documented in the contract are set conservatively, or the contract ‘protection’ is available to the builder to accommodate continuing experiences of supply chain disruption.

Mitigating damage on existing commitments

The impact of delays and inflation on materials over the last 6 months is likely to render many projects committed as fixed arrangements prior to then as unprofitable for builders. Quantifying the likely financial impact of delays in terms of lost margin, burnt overhead and people costs, along with potential damages exposure to principals can be a challenge, but scenario modelling the likely impact on the business will support strategies to:

- Update project delivery plans to ensure key materials (such as framing) are ordered sufficiently in advance;

- Consider assuming responsibility for key material supplies from subcontractors (such as framing) if concerns exist as to the capacity of subcontractors to deliver on time;

- Encourage transparent dialogue with key subcontractors and suppliers so that emerging issues are dealt with proactively rather than reactively.

- Ensure risk points are raised during PCG (Project Control Group) meetings;

- Negotiate variations of contract terms, consider reasonable delay buffers where external factors persist;

- Bulk order materials in short supply – where available;

- Engage with financiers to ensure continuity of existing facilities critical to future operations (e.g. bank guarantees and equipment finance);

- Maintain liquidity (including securing fresh debt or equity funding); and

- Ensure the business remains compliant with regulatory covenants (QBCC-MFR and Government Pre-Qualified Contractors).

Ensuring the business is protected on new projects (in addition to the above)

- Provide shorter turnaround time on the validity of quotations;

- Explore options to contract on a cost-plus basis/ schedule of rates (is possible);

- Nominate at-risk materials to be subject to cost-escalation clause; and

- Incorporate further protections in contracts (extensions of time, contingent start date based on availability of materials).

How can we help?

The team at Grant Thornton Australia can offer its expertise to assist builders, developers, financiers or other key stakeholders navigate distress, in various ways:

- Quantifying the financial impact of these market factors on business cash flow;

- Connecting data provided by quality surveyors to create dynamic cash flow forecasts, specified to contract terms and the pipeline of specific businesses;

- Assist in securing finance to improve working capital, via debtor financiers, alternate debt or extension of existing bank facilities;

- Assist negotiating with key counterparties, such as the ATO, contract principals or sub-contractors; and

- Managing regulatory compliance with bodies like the QBCC or State Government pre-qualifications.

While price volatility and risk presents a major challenge for builders, developers and financiers alike, the exploding lead times and delays of materials contribute to further headaches. It may get worse for some materials before it gets better. The contrasting outcomes for businesses that reactively vs proactively manage these risks are likely to be stark.

COVID building boom: who’s likely to be stung?

1 ‘Unprecedented times’ for ocean freight as fees soar

2 Economist - September 18-24th 2021 (Page 63)

Supply chain risk management in the COVID building boom

Watch this webinar on-demand as we host a panel discussion on the ways businesses are responding to supply chain challenges and when supply/demand may return to normal – if at all.

Watch on-demand now