Fintechs – which range from digital only banks to any technology used to streamline, digitise or disrupt traditional financial services – are emerging in response to the rapid rise of Australians' demanding 24/7 access to their banks.

This is enabled by their systems – Software-as-a-Service is considerably cheaper and more nimble than legacy systems – and they will be heavily reliant on technology and innovation to ensure they remain relevant, secure, and responsive to trends in customer needs and demands.

volt bank Limited received Australia’s first Restricted Authorised Deposit Taking Institute (RADI) licence in 2018 – the first new retail-focused bank licenced since the early 2000s.

COVID is but a blip

In the lead up to COVID-19 we saw some exciting new moves in the marketplace with three neobanks granted licences by APRA. The neobanks offer alternatives to traditional banking in that they are online only – but come with the need to build a customer base and generate capital, something that may have been a struggle as world economies adjusted to a global health crisis.

Unsurprisingly, APRA made the decision to delay the issuance of new banking licenses from March 2020 through to March 2021. In the background, fintechs have been busy further developing their product offerings and APRA applications. APRA also released its revised approach to licensing and supervising new ADIs in August 2021 which provides guidance for new ADI entrants. Since the suspension on new licences has been lifted, we’ve already seen Alex Bank granted a licence as a restricted authorised deposit-taking institution – the first in more than one and a half years.

With even the traditional banks moving increasingly online, customer confidence in online banking will only increase – leading to more customers looking to digital and online only banks as genuine alternatives to the Big Banks. Not only was COVID just a blip, but it’s also created a larger market for the sector.

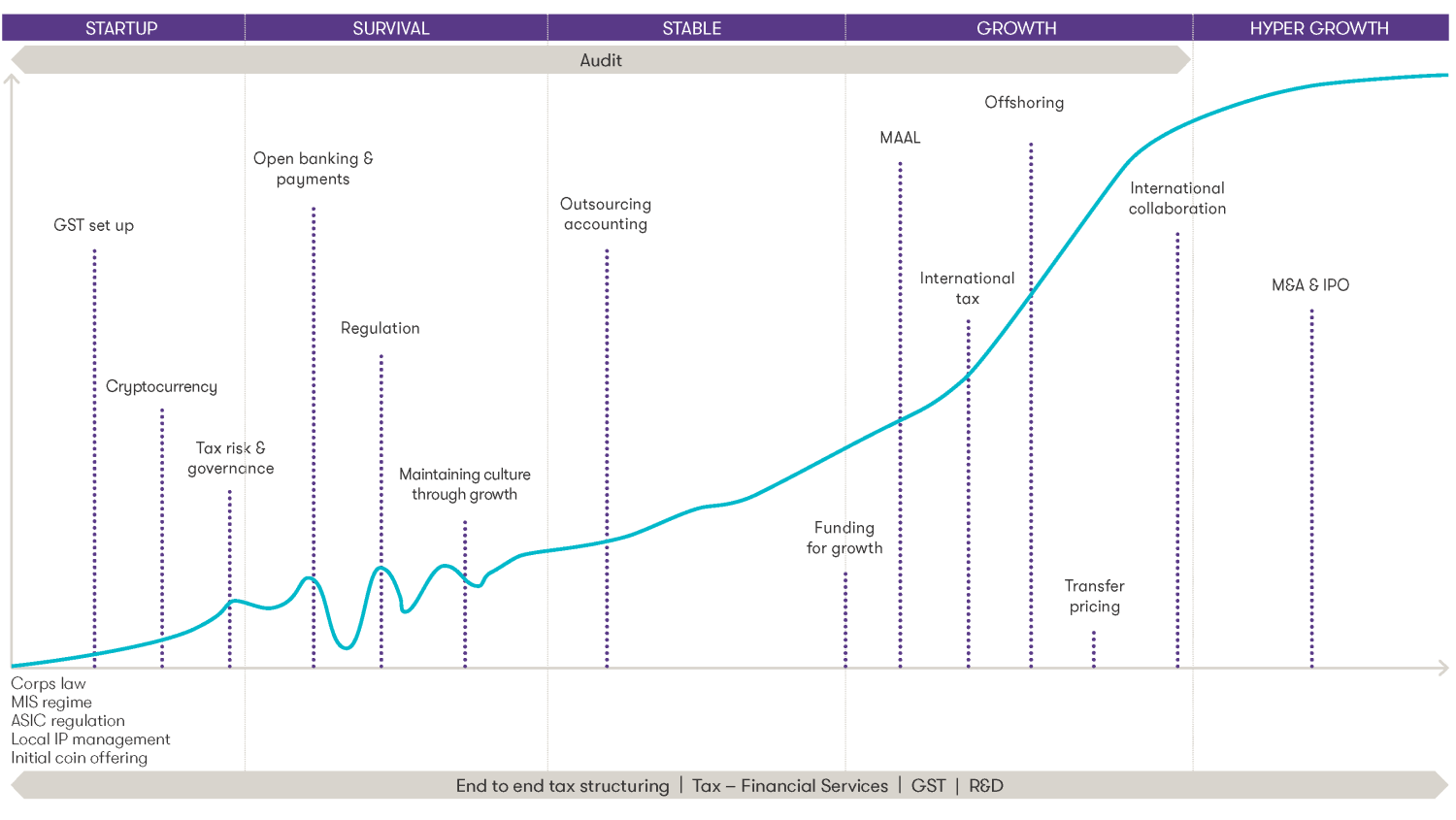

The fintech lifecycle

The lifecycle of a Fintech may start with an innovative and digital first concept, but may be underpinned with regulation, governance and a strong growth strategy. It’s important to have advisors in place that understand the sector – as we know, technology moves significantly faster than tax reform and many jurisdictions are still trying to figure out how they regulate and tax the digital economy.

![gtal_2019_fintech_lifecycle.png]()

Here in Australia there are a number of inquiries including a Senate Fintech inquiry by the “Committee on Australia as a Technology and Financial Centre” and the RBA’s investigation into a Central Bank digital currency. Both has the potential to further (and completely) disrupt the financial services sector – and hopefully provide the platform for new entrants and competition in the fintech space.

Research and development will be an ongoing and constant requirement for these new entrants. The new banking landscape will be fast paced, adaptable and agile – our regulation needs to match. The trick will be ensure we have the right regulatory settings to allow fintech and neobanks to establish, thrive, and continually innovate.