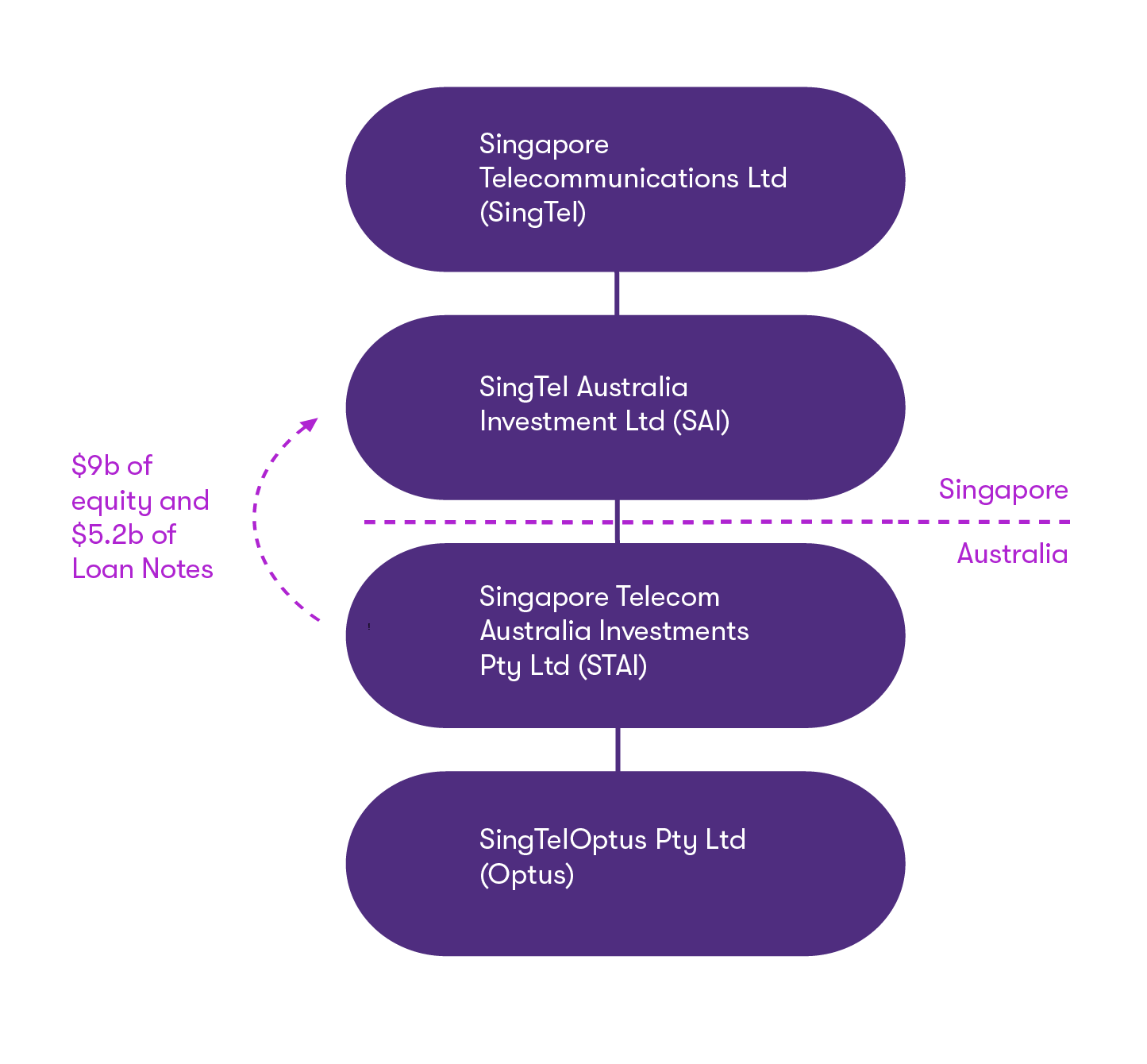

Singapore Telecom Australia Investments Pty Ltd’s (STAI) appeal was dismissed by the Full Federal Court last month.

Contents

This outcome highlights the Australian Taxation Office’s (ATO) focus on multinational tax avoidance through debt funding arrangements to engage in transfer mispricing. Further, it provides valuable insights on key factors that should be considered and documented when pricing cross-border financing arrangements.

STAI was found to owe the ATO approximately $268m in tax (and an additional $125m in interest and penalties). This tax liability arose from the $895m in debt deductions that had been claimed by STAI for interest payments made from 2010 to 2013 on a cross-border financing arrangement with an offshore related party.

In the decision handed down on 8 March 2024, the primary judge agreed with the Commissioner that the debt funding arrangement had been structured in a way that resulted in STAI paying excessive amounts of interest than would have been expected had the parties been dealing at arm’s length. The SingTel Group was therefore found to have obtained a transfer pricing benefit via their debt deductions.

The facts

In October of 2001, SingTel Australia Investments Ltd (SAI) located in Singapore acquired an Australian telecommunications business now known as SingTelOptus Pty Ltd (Optus). The decision was subsequently made to change the holding structure of Optus, and in June of 2022, SAI sold all of its shares in the Optus business to STAI. STAI’s acquisition of 100 per cent of the issued share capital was funded through a combination of debt and equity, and for the purposes of this article, we will focus on the debt component (namely, $5.2b of Loan Notes).

A Loan Note Issuance Agreement (LNIA) was entered into between SAI and STAI under which the amount of $5.2b was advanced. The initial terms of the LNIA were such that the Loan Notes were denominated in AUD with a tenor of 10 years. The interest rate payable was a floating rate of 1 year Bank Bill Swap Rate (BBSW) plus 1 per cent per annum (grossed up for withholding tax).

The LNIA also carried a unique term stating interest payments were not required by STAI until a ‘variation notice’ had been issued by SAI. SAI could effectively determine when, over the 10-year term of the LNIA, STAI was required to pay interest and in what amount. However, under the terms of the LNIA, the liability to pay interest still accrued. It was the timing of the obligation to make payment which could be deferred.

The LNIA was amended on three occasions, as outlined below:

On 31 December 2002, the maturity date was reduced by one day.

On 31 March 2003, the terms were changed with retrospective effect such that interest was only accrued and payable once certain benchmarks relating to Optus’ financial performance were met. The interest rate was also increased by adding a ‘premium’ of 4.552 per cent.

On 30 March 2009, the floating interest rate of rate of 1-year BBSW was amended to a fixed interest rate of approximately 6.835 per cent. The effective interest rate after the 1.000 per cent margin, the 4.552 per cent premium and the withholding tax gross-up was 13.27 per cent.

On 28 October 2016, The Commissioner issued STAI with notices of amended assessments based on transfer pricing determinations made under Division 13 of the Income Tax Assessment Act 1936 (“ITAA 1936”) and Subdivision 815-A of the Income Tax Assessment Act 1997 (“ITAA 1997”) for each of the 2011, 2012, and 2013 tax years. The object of these amended assessments was to disallow approximately AUD 895 million in interest deductions. These were objected to by STAI in December 2016. When The Commissioner denied STAI’s objections, STAI took the matter to Court. On 17 December 2021, the Federal Court found in favour of The Commissioner

Grounds of appeal

STAI lodged an appeal against the original decision of the primary judge. Of note, STAI’s appeal was put forth on the comprehensive basis of 49 separate appeal grounds that were grouped into seven alleged errors. While we will not go into further detail around the separate appeal grounds, in the decision that was handed down on 8 March 2024, all grounds of appeal were dismissed by the Full Federal Court.

The key takeaways or findings from this case are outlined below:

Key findings

The primary judge noted that the amendments made to the LNIA in 2003 and 2009 lacked commercial rationale, and independent parties were unlikely to have agreed to these. More specifically:

The 2003 amendment imposed a profitability benchmark which exposed both parties to commercial risk i.e., STAI may never have reached the required profitability and could therefore have avoided interest payments for the entire tenor of the loan, or alternatively STAI may have reached the required profitability earlier than accounted for and therefore paid an excessive amount of interest. Further, the 2003 amendment resulted in SAI forgiving approximately $286m of accrued interest, an amount which is unlikely to have been forgiven in similar circumstances between independent parties.

An independent party in the same position as STAI was unlikely to have agreed to the 2009 amendment to change the 1-year BBSW rate to a fixed rate of 6.835 per cent given the floating rates were dropping at the time and the transaction only had 3.5 years left to run.

The above reiterated the importance of having regard to the arm’s length principle when pricing transactions, and echoed the importance of commercial realism and consideration of whether independent parties would enter into the same or similar arrangements.

The transfer pricing provisions in Division 13 of the ITAA 1936 and Subdivision 815-A of the ITAA 1997 both require the use of ‘hypotheticals’ to ascertain whether the interest amounts paid by STAI to SAI were arm’s length and if not, then to determine the quantum of any transfer pricing adjustments. This is done by seeking to understand what independent parties in the positions of STAI and SAI might have been expected to have done. In the SingTel decision, it was confirmed that the hypothesis should be as close as possible to the actual terms of the arrangement or characteristics of the parties in question.

The primary judge noted that a number of factors are taken into account by credit rating agencies such as Standard & Poor’s and Moody’s when determining the credit rating of a subsidiary. Such factors include implicit parental support, business risk, and financial risk. Notably, this idea of increased creditworthiness for subsidiaries due to group membership is not new and the SingTel outcome confirmed the ATO’s view that parental affiliation should be considered when pricing debt.

Further to the point above, the primary judge noted that given the size of the loan, the general expectation of independent lenders to obtain a security particularly for a borrowing of this size, and the fact that SingTel had provided a parent guarantee for a bank facility for another subsidiary in the Group in the month before the LNIA was entered into, all assisted in indicating that an explicit guarantee might have reasonably been expected to be included in the LNIA. Further, expert evidence illustrated a parent guarantee was likely to have significantly decreased the interest rate on the loan, which an independent parent company in SingTel’s position would reasonably have leveraged to ensure a reduced overall borrowing cost for the Group.

In addition, the idea of whether the issuance of a parental guarantee (explicit or implicit) should attract an arm’s length guarantee fee was discussed. While the verdict in this case was that there was insufficient evidence to conclude a guarantee fee might reasonably have been expected to be paid by STAI to its parent, this case affirmed there may be instances guarantees should incur a separate additional fee.

When the LNIA was entered into, the interest liability pertaining to the arrangement could be deferred and capitalised, and withholding tax was therefore payable by STAI in Australia in relation to the accrued interest amount. When the 2003 amendment was put through, the benchmark which was introduced deferred the accrual of interest. The Court concluded there did not appear to be any commercial rationale for the 2003 amendment, apart from to avoid the payment of withholding tax (at least for a time). This was not considered further in the case given the definition of a transfer pricing benefit in Subdivision 815-A is more narrowly defined than Subdivision 815-B and does not consider underpayment of withholding tax. The Commissioner may arrive at a different outcome should an assessment be made under Subdivision 815-B.

It was confirmed that Subdivision 815-A of the ITAA 1997 operates in a way that delineates the amounts of profits corresponding with a particular income year, as opposed to profits accrued over the totality of the arrangement. To clarify, where an intercompany arrangement spans 10 years for example, the outcome at the end of each income year should be assessed to confirm whether any transfer pricing benefit has arisen as opposed to the outcome at the end of the 10-year period.

Recommendations for impacted taxpayers

All taxpayers with existing cross-border financing arrangements or taxpayers considering entering into intragroup debt funding arrangements should take heed of this outcome, and:

Seek appropriate advice when setting the terms and conditions of their agreements as the Court has shown they place significant reliance on this.

Frequently review their debt funding arrangements to ensure the terms and conditions documented reflect the commercial substance of the arrangement.

Ensure any amendments to intercompany loan agreements can be commercially rationalised and are contemporaneously documented to illustrate and support that independent parties would have accepted similar amendments in the same or similar circumstances.

Consider implementing a policy with respect to parent company guarantees, borrowing at the lowest available cost of funds (where this is commercially rational), and explicit support.

Maintain evidence of the commerciality of intragroup debt funding arrangements.

Concluding remarks

While the ATO had previously identified intragroup debt funding as a high focus area, this landmark outcome in addition to other landmark cases such as Chevron and Glencore, continue to highlight the importance of multinationals performing a two-sided analysis to ensure intercompany arrangements are commercially rational for all parties to the arrangement. Further, the outcome reaffirms the value placed by the Court and ATO on taxpayers having contemporaneous documentation to evidence or support their transfer pricing positions. It is therefore integral for taxpayers to seek appropriate advice when setting the terms and conditions of their agreements, and to review their transfer pricing arrangements annually.

We’re here to help

Please contact Jason Casas, Christine Cornish, Keith To, or Arani Ganendren if you wish to discuss the above or the broader implications of this outcome further.

With the 30 April 2026 registration deadline approaching, companies that performed R&D activities in the year ended 30 June 2025 should be reviewing eligibility, documentation and governance now to preserve their entitlement under the RDTI.

Subscribe now to be kept up-to-date with timely and relevant insights, unique to the nature of your business, your areas of interest and the industry in which you operate.