The first bank in Australia, Bank of New South Wales, was established more than 200 years ago in 1817. This was followed by more banks in the 1830s and 1850s as the country grew. It was completely unregulated and speculative, but the banks even back then were underwriters for economic activity.

Move forward to today and the Australian financial services sector is performing the same function but within a controlled environment to protect both the banks and consumers from anticipated and unanticipated shocks to the economy. And what a shock we have had in 2020. Bushfires, a pandemic and now a recession.

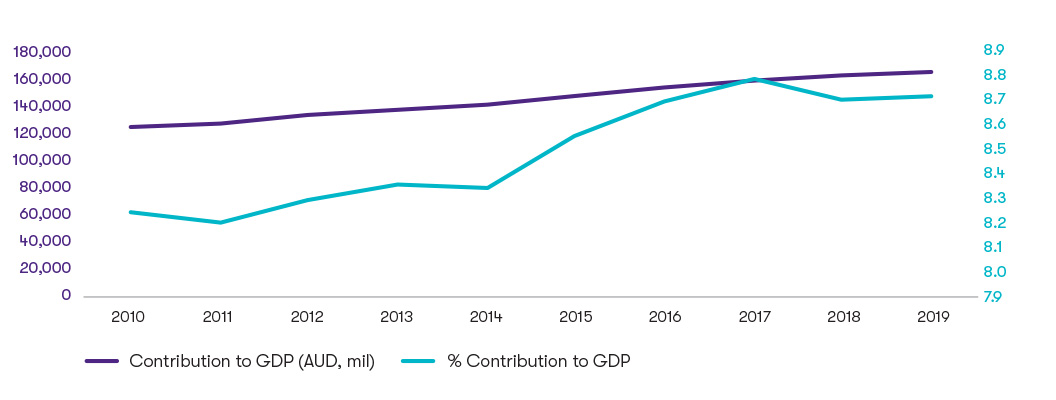

Banks and the wider financial services sector are underwriters for economic activity. In pulling our ‘Federal Budget: A 10 year retrospective’ report together we knew we had to look at financial services differently as the sector is, in many ways, a tool in the policy makers toolkit to support the economy. The Government then doesn’t invest in financial services the same way it does the energy sector or the health sector. But it does heavily regulate and monitor what is actually one of the largest contributors to GDP in our report.![GTAL_2020_FS_FB_Graph.jpg]()

The sector will continue to act as the “shock absorber”

We are not out of the recession yet. It may take years, and financial services institutions will continue to play an important role in growing out of the recession. In addition to providing support, there is also continued reform happening within the sector. For instance, there were important changes to superannuation in the Budget. From a consumer perspective this is a positive move. From a backend perspective, this will add an additional layer of administrative burden that was already under pressure from the superannuation early access initiative from earlier this year. There is capital flowing, but it must be paired with reporting and oversight.

While our financial services sector is strong and resilient it cannot be viewed as a bottomless pit. If banks erode their capital to provide support for borrowers experiencing hardship due to COVID-19, they will need time and resources to build up their capital levels post COVID.

In our report we cover:

- The economic underwriters

- The sector bends and flexes in response to the economic crisis

- Competition stifled?

- What about general insurance?

- Megatrends are moving faster

- So where to from here?

![GTAL_2020_Federal-Budget-2020-21.jpg]()

Looking back to look forward

We were initially writing the ‘Federal Budget: A 10 year retrospective’ report before COVID-19 as an advocacy piece for more industry investment and support. Of course, the way the year started is not the way the year is ending. Many sectors that had been left to their own devices are now key for our recovery. Sovereign capability. Jobs. Digital economy. Modern manufacturing. Renewable future. Deregulation. Innovation. These are the terms we will use as we settle into COVID-normal.

Our report looks retrospectively at 13 different industries, the investment made into them by Government and their contribution to GDP. This is then overlaid with the opportunity we see for industry in this new normal based on recent Government announcements.

Download report