The Government’s media release proposes the following phased approach to rolling-out PBA’s:

- “From 1 July 2020, the Queensland Government proposes to expand the PBA system through a phased approach to give plenty of time for the industry to prepare and have new administrative procedures in place, minimising financial stress.

- Within 24 months, PBAs will apply to all Queensland building projects valued at over $1 million.”

The Government plans to firstly expand the application of PBAs to larger government projects, and then to private sector projects. The Queensland Government accepted, or accepted in-principle, all 20 recommendations from the Building Industry Fairness Reforms Implementation and Evaluation Panel Report regarding Project Bank Accounts (PBAs).

Based on the release and the Government’s response to the recommendations of the PBA evaluation panel, the expanded roll-out (beyond the Phase 1 status quo) may be:

|

Phase 2

1 July 2020

|

Application to all Qld State Government building projects above $1m

|

|

Phase 3

1 July 2021

|

Application to all building projects (including private) in Qld above $10m

|

|

Phase 4

1 January 2022

|

Application to all building projects above $3m

|

|

Phase 5

1 July 2022

|

Application to all building projects above $1m

|

The report, which proposed amendments to the Building Industry Fairness (Security of Payment) Act 2017 (BIF Act), outlined the industry’s suggestions on the practicalities of the proposed changes to the use of PBAs

Background

Project Bank Accounts are a key component of the Queensland Government’s security of payment reforms, which were trialled from 2018 for Government building contracts between $1 million and $10 million.

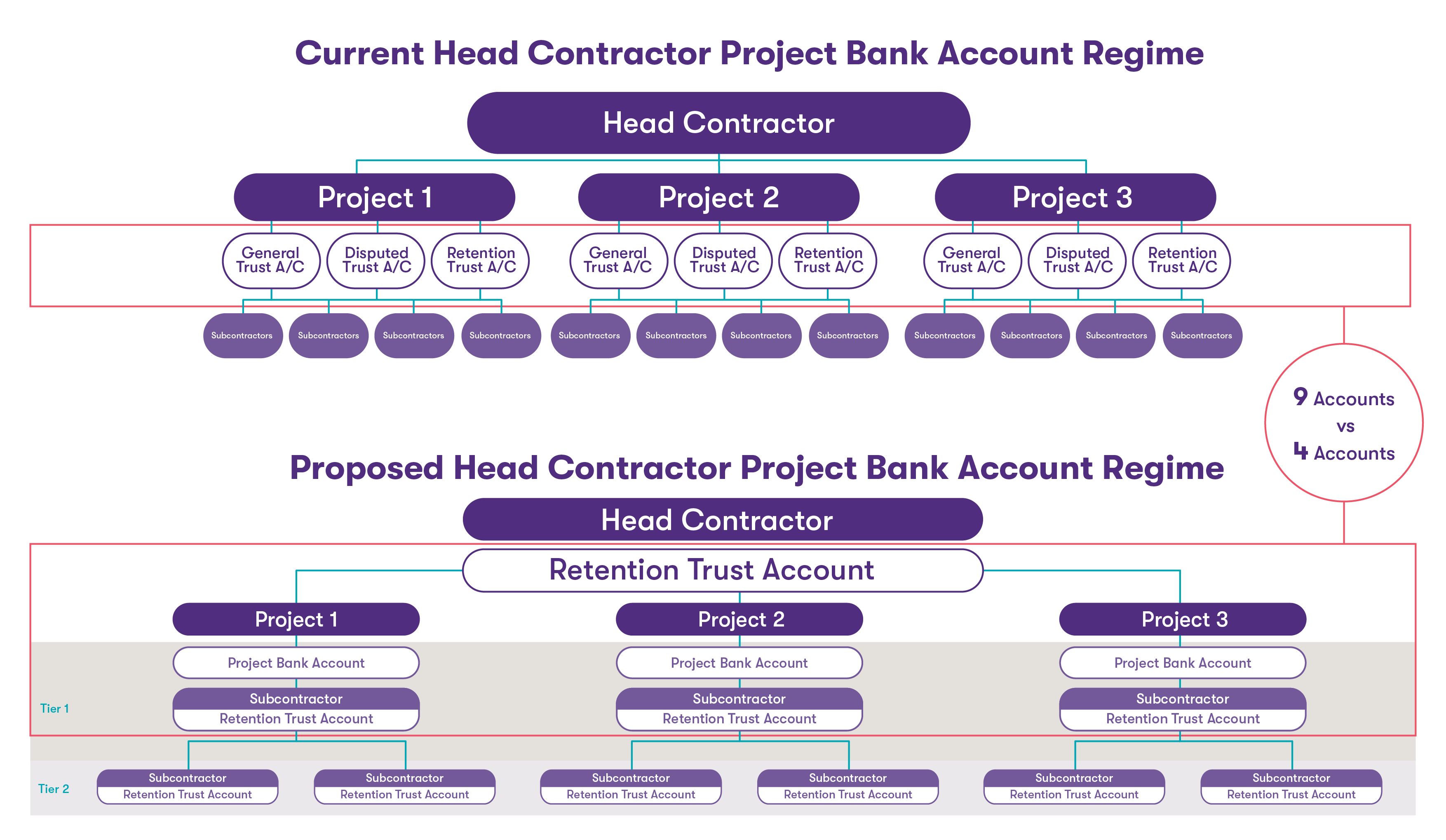

Currently, the legislation requires that head contractors establish the following 3 trust accounts for each qualifying project to secure monies for the benefit of subcontractors:

- general project account

- retention account

- disputed monies

Changes to Retention Monies Trust Account

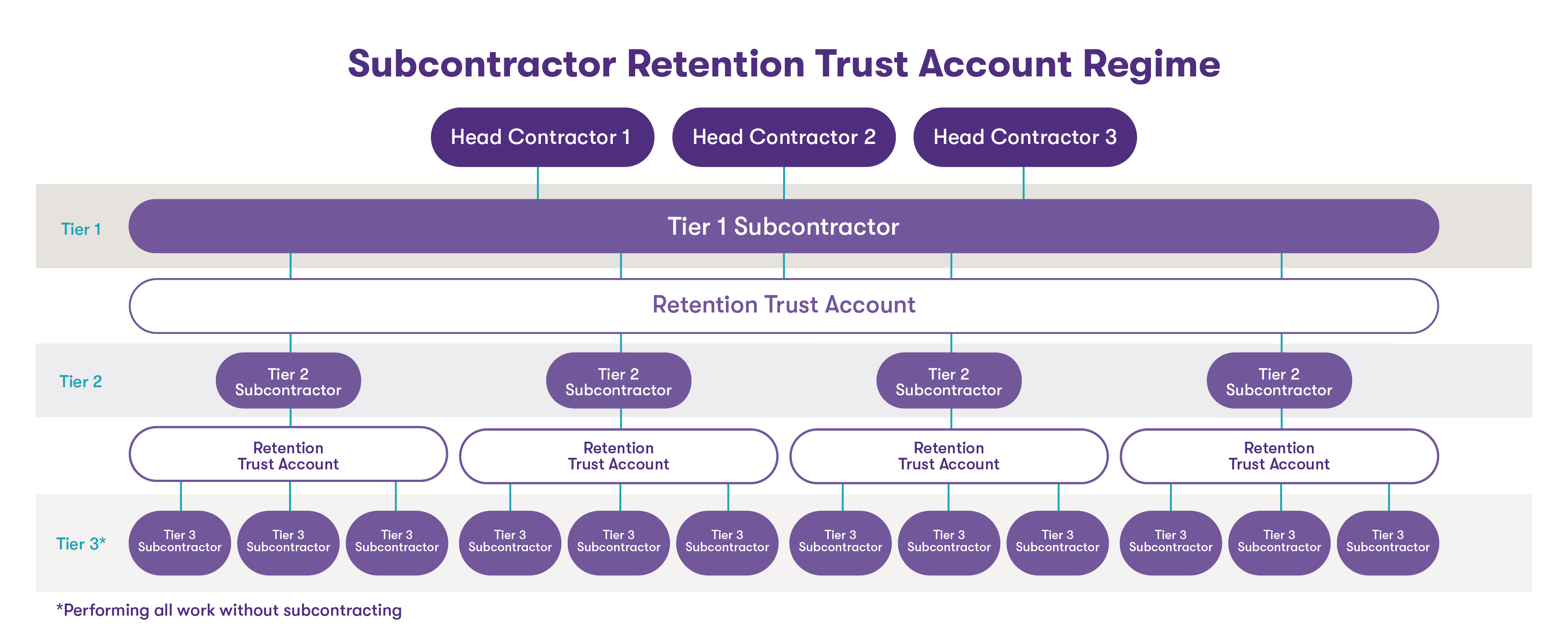

- Head contractors will now be able to maintain a single retention monies trust account for all subcontractor retentions which is in contrast to the current regime where separate retention monies trust accounts are required for each project.

- The obligation to operate a single retention trust account will now extend to all building and construction contractors (including all levels of subcontractors) and private sector principals. This obligation is decoupled from the requirement to establish a PBA.

- Mandatory external reviews will be required initially within the first 6 months of a retention trust account being opened and continue annually thereafter. While the Government has indicated a desire to minimise the administrative burden of the regime by aligning any such reviews with existing financial audit requirements, businesses below the audit threshold ($50m turnover FY20) will still face an additional administrative burden.

- Prior to opening a trust account, contractors wishing to hold cash retentions will be required to complete training and assessment by an approved training provider to ensure that they fully understand their role a trustee, accounting, record keeping and other obligations (similar to real estate and auctioneers).

- The roll-out of retention monies trust accounts will be phased, as with PBA’s.

Changes to Disputed Monies Trust Accounts

- The requirement to open and maintain a disputed monies trust account for each project will be abolished. This is not surprising as under the current drafting, this account was of limited assistance to subcontractors with disputed claims.

Other changes

- The Government proposes improving security of payment for all contractors (including head contractors) by introducing “payment withholding requests”.

- Subcontractors will be able to issue payment withholding requests to principals on or after making an adjudication application, to protect disputed amounts and reduce the risk of nonpayment following adjudication.

These changes are intended to also apply to projects that do not require a PBA and will provide an ability to “issue a charging order or impose a lien over property”. With Queensland being the first jurisdiction to introduce such measures, the changes will provide expanded protection for head contractors from failure by developers/ principals.

Key changes: Good news for head contractors

- A single retention monies trust account will be sufficient to deal with all subcontractor retentions – this means less administration for contractors.

- The requirement to open a disputed monies trust account for each project will be abolished – both of these measures are likely to be good news for the banks as well as head contractors.

- Improved security of payment will give the ability to “issue a charging order or impose a lien over property”, providing expanded protection for head contractors from failure by developers/principals and will apply to both PBA and non PBA projects.

![GTAL_2020_REC_Current_PBA_Regime.png]()

Click to enlarge

Key changes: Bad news for mid-tree subcontractors and principals

- Expanded obligations to operate retention trust accounts now extend to all building and construction contractors (including all levels of subcontractors) and private sector principals. This obligation is separate to the requirement to establish a PBA.

- Mandatory external trust account reviews will be required initially within the first 6 months of a retention trust account being opened and continue annually thereafter – creating additional compliance burdens from businesses below the audit threshold.

- Contractors wishing to hold cash retentions in a Trust Account will be required to complete training and assessment by an approved training provider.

![GTAL_2020_REC_Subcontract_RTA_Regime.png]()

Click to enlarge

Implications for business

The Government has acknowledged that the “removal of project and retention funds from operating capital is an intended consequence of the reforms and some businesses may need to change their financial management practices and find other sources of working capital from savings, by increasing debt, or liquidating assets” and suggested that the phased roll-out will provide “sufficient time for market adjustment”. The message to those businesses who will be effected by PBA’s is to consider the cashflow impact on your business well in advance of commencement.

Look out for

The Government has indicated a desire to amend the BIFA to enable the expansion of the regime to require subcontractors (2nd tier contractors) to establish PBA’s where prescribed by Regulation. According to the Government’s Building Industry Fairness Reforms Implementation and Evaluation Panel Report, this “will allow government to monitor and respond quickly and effectively to ensure avoidance practices do not undermine the integrity of the PBA framework”.