In Commissioner of Taxation v Bendel [2026] HCA 18, the Court found by a 5:2 majority in the taxpayer’s favour, ruling that a UPE resulting from a trust appointing income to a corporate beneficiary does not constitute a ‘loan’ for Division 7A purposes. The Court’s decision affirms the earlier decisions of the Full Federal Court and the Administrative Appeals Tribunal (now the Administrative Review Tribunal).

The majority decision

The majority ruling found against the ATO’s long-held position that a UPE between a trust and an associated company was regarded as a 'loan' for Division 7A purposes. It was held that a UPE was neither a loan in the ordinary sense and nor taken to be a ‘loan’ in accordance with the expanded definition of the term in Division 7A. The Court drew Parliament’s intention from Division 7A’s legislative history and particularly that another part of Division 7A, Subdivision EA, was written to cover the situations like the Bendel case.

Such a basis is not new. It has been evident in 2009/10 – when the ATO’s views first emerged – and all times since that provisions designed for a specific situation should be allowed to operate as intended, rather than other provisions being revisited or reinterpreted in a way that diminishes their effect.

What it means for private business owners

This decision is likely to have a broad impact, but the practical implications and actions to take are not clear at this early stage.

Most affected taxpayers since the 2009/10 change in interpretation have complied with the ATO’s position, given the potential if not aligned for the ATO to assess deemed unfranked dividends under Division 7A.

This has meant executing documents to govern arrangements (eg a ‘sub-trust agreement or complying loan agreement’) between the trust and corporate beneficiary in line with the ATO’s views, with the trust making payments of interest and principal (if required) to the corporate beneficiary. The administration of such arrangements placed strain on trust structures and their controllers to find cash to enable progressive discharge of UPEs, and distribution of the related funds as dividends to shareholders of the private companies.

The practical outcome from complying with the ATO’s position for many private business owners has been to incur ‘top-up’ tax – being the balance of tax from the company tax rate up to the owners’ personal marginal tax rate – including on profits they have not yet drawn, but have retained and reinvested in their business or other trust assets.

While the High Court’s decision might be welcome news for private groups in these situations, it is not a case of simply ceasing to continue with the past practices under the Commissioner’s approach. For example, where past years’ UPEs have been converted to a loan under a complying loan agreement, those documents need to be implemented in accordance with their terms, leaving such loans as still being subject to Division 7A rules. There will be some groups where the complexity of their structure and their arrangements make it difficult to conclude precisely how the Bendel case affects them in practice.

Further, UPEs that continue to remain unpaid could lead to other rules applying, including:

- Subdivision EA of Division 7A can impact where trusts with UPEs to associated companies undertake loans, certain types of payments, and debt forgiveness transactions with associated parties.

- Section 100A which applies to so-called reimbursement agreements, produces an outcome potentially more adverse than Division 7A, as a flat 47 per cent tax rate applies. Despite section 100A being enacted in 1979 and directed at different situations, ATO officials have regularly reminded tax advisers that they consider that section 100A could potentially apply in these situations if Division 7A is found not to apply. Their view broadly is that they will not apply section 100A where distributions are paid in cash to the nominated beneficiaries, a view that is yet to be tested.

- Part IVA the general anti-avoidance rule.

The following examples highlight how the Bendel decision does not necessarily relieve the compliance burden:

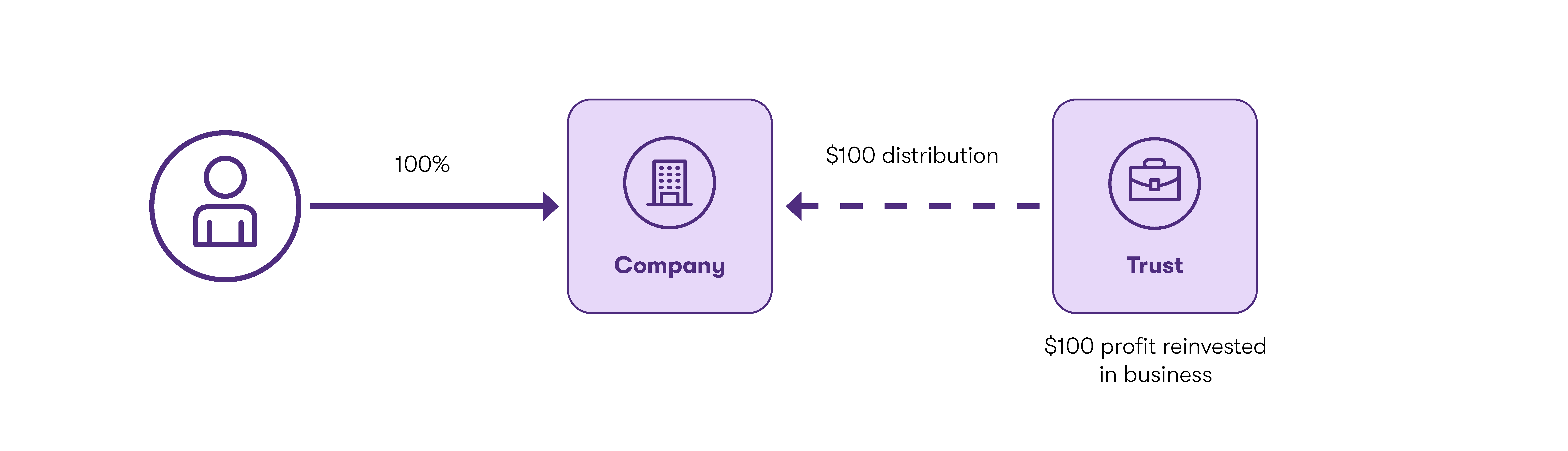

Example 1

A trust makes a profit that is reinvested in its business. The profit is allocated to a company, and the profit is taxed at the corporate tax rate (at either 25 per cent or 30 per cent depending on whether the company is a base rate entity).

The profit is not distributed, so remains a UPE.

The trust has applied the funds in a manner that does not activate Subdivision EA, so no deemed dividend would arise.

If the ATO considers that section 100A ought to apply instead, the trustee will pay tax at a rate of 47 per cent. ATO guidelines infer that non-payment of distributions would bring section 100A within scope.

![]()

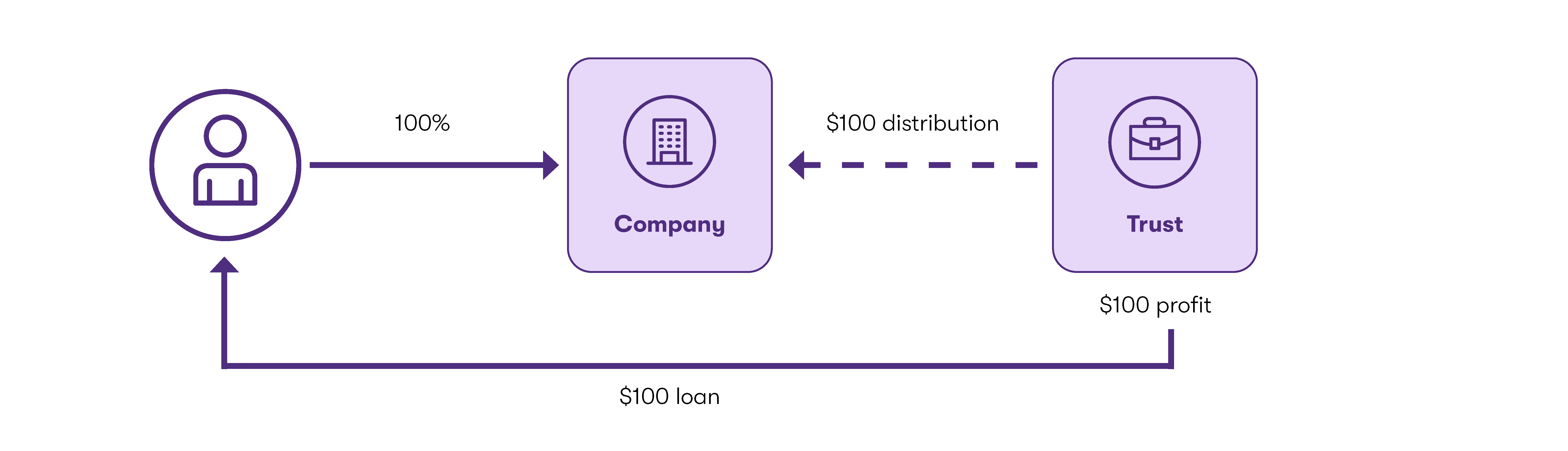

Example 2

Consider the same situation, but instead the trust profit is lent to the company’s shareholder.

This situation would activate Subdivision EA. As such, unless the loan was repaid or documented on Division 7A complying loan terms, the loan amount will be taxed as a deemed dividend to the individual. In such situations, many people would document the loan on Division 7A complying loan terms so that it can be managed over time.

The residual question is whether section 100A might also apply. It should be reasonable to conclude that Subdivision EA is doing its job and other provisions, especially those that pre-dated Division 7A, should not apply.

![]()

The contrast between the two examples highlights how outcomes can vary significantly, depending on which provision the Commissioner might apply to a situation. This creates a risk that an action like reinvestment in a business could result in a punitive tax outcome and one worse than making a loan to an associated party.

What happens next

Trustees need to make their distribution decisions for the year ended 30 June 2026, despite the uncertainty raised by this Court finding.

The Commissioner will release a Decision Impact Statement to explain how the ATO considers taxpayers affected by the decision should respond. Of particular interest will be whether the ATO will elevate the role that section 100A might play, a view that itself will almost certainly lead to challenge.

Legislative reform is necessary. A situation of no further action by Government is implausible and the recent Budget’s focus on trusts creates an environment where reform is possible. Accordingly, what might follow includes:

- Revisiting the proposed reforms to Division 7A that were announced in the 2018-19 Federal Budget, which included legislating for the inclusion of UPEs into the definition of ‘loan’. In this case, taxpayers would essentially continue with current practices under the ATO’s approach, but backed by statute.

- Considering other reforms to the taxation of trusts, including the entity taxation proposal flagged in 1999/2000.

Budget announcement affecting corporate beneficiaries

As previously communicated, the Government intends to legislate a 30 per cent tax on discretionary trusts from 1 July 2028, for which a corporate beneficiary will not be permitted a credit. If enacted, this will produce double-taxation and effectively means that the use of corporate beneficiaries will become unviable from that date.

As a result, appointing trust income to a corporate beneficiary might be viable for only a further three income years (i.e. years ending 30 June 2026, 2027 and 2028).

Trust income appointment decisions for 30 June 2026 income year

We are currently approaching the end of the 30 June 2026 income year, in which trustees make the annual resolutions for appointing trust income. The question arises to whether you now should do anything differently. The short answer is ‘no’.

We recommend that resolutions to appoint trust income for the 2025-26 income year be made after applying the usual considerations in the ordinary manner, including appointing to a corporate beneficiary if that is optimum and appropriate. Whether the UPEs arising are to be, or not to be, converted to a loan is a matter to be decided at a later time when there is greater clarity.

What about corporate UPEs arising for the 30 June 2025 year?

This is also the case for UPEs with corporate beneficiaries arising for the 2024-25 income year. Unless they change their interpretation, under the ATO’s approach, these became a loan during the 2025-26 income year, meaning you have until before the lodgement day for the 2025-26 income tax return to convert to a complying Division 7A loan. Although that is not required as the law stands right now, we reiterate that there will almost certainly be a response from government and/or Parliament. The point again is that immediate action is not required, and there will be time to assess what is to be done.

As noted above, it will remain to be seen how the arms of government respond, but there is every reason to continue using corporate beneficiaries for 2025-26 in the usual manner.

We will continue to monitor developments as they unfold and will return to this significant matter in due course.

Please contact your trusted Grant Thornton advisor to discuss these developments, especially if you are directly affected by the decision.