AASB 15 replaces the legacy revenue guidance contained in multiple places (in particular AASB 118 Revenue) as the accounting standard applied to the majority of commercial transactions with customers.

The relatively general wording of AASB 118 resulted in significant disparity in practice for entities entering into transactions with similar economics – AASB 15 introduces a common framework for revenues to apply when recognising revenue, while also changing the decision process for determining 'principal' and 'agent' relationships.

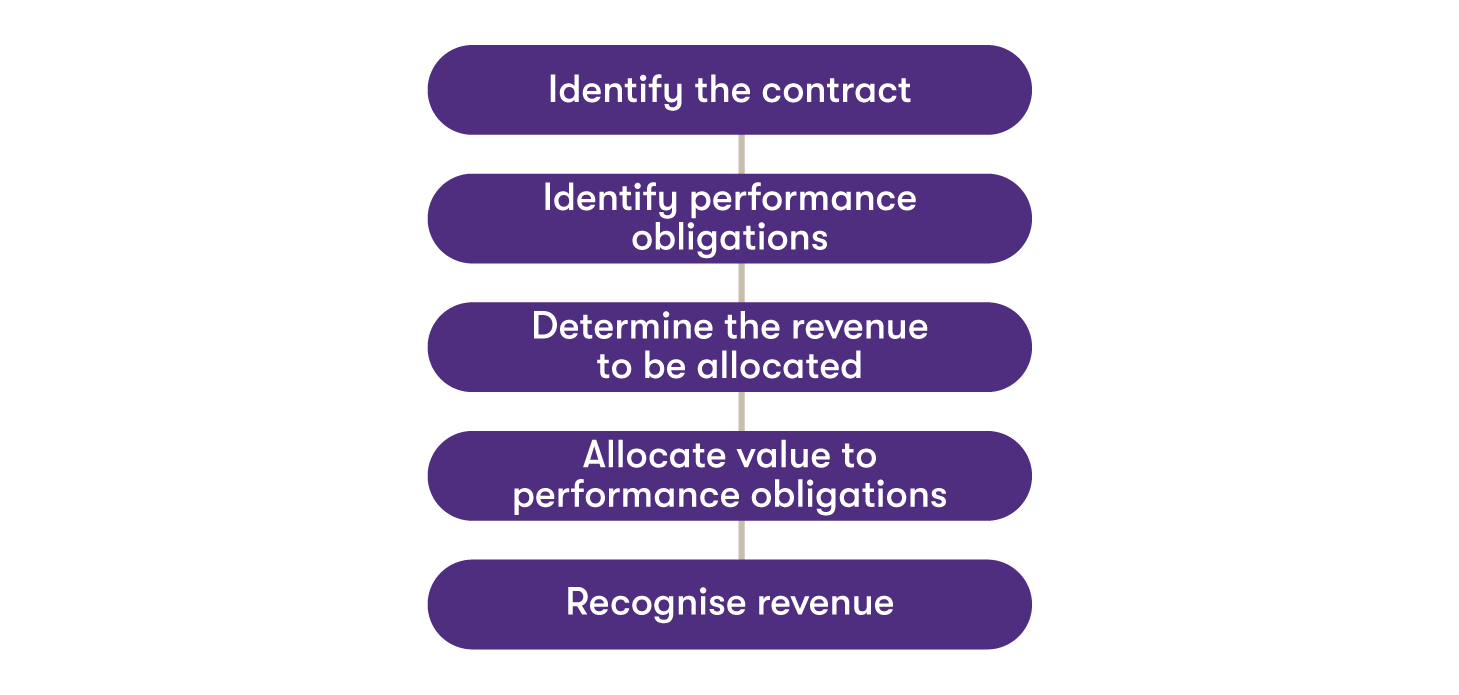

The common framework – typically referred to as 'The Five-Step Model' – requires that an entity:

![AASB 15 Revenue]()

While a seemingly simple progression from one step to the next, additional complexity is introduced at each step, including:

- grouping of contracts

- differentiating in a contract between 'promises' and 'performance obligations'

- measuring non-fixed consideration

- measuring the relative values of each performance obligation

- determining whether revenue is recognised at a point in time or overtime, and the most appropriate method of recognising revenue over time.

How we help

Revenue transactions are recurring in nature. Any advice must address the technical ramifications of a contract or series of contracts to ensure technical accuracy, and result in policies and procedures that can be consistently and quickly applied to the financial information you generate.

Our team has multiple years of experience in applying the new framework to complex revenue recognition situations, prioritising simple and reusable outcomes.

We can help you by:

- developing technical white papers

- drafting revenue accounting policies

- providing guidance in developing models or systems to assist in the accounting for revenue.

For some, the complexity of AASB 15 has resulted in errors in the initial application, especially where a formal assessment was not undertaken. Contracts of a new form — for example, with new revenue arrangements and/or for previously undelivered goods and services — may introduce additional complexity not previously considered.

We are commonly asked to assist with:

- applying AASB 15 when other standards take precedent — especially AASB 16 Leases

- measuring revenue in the presence of other contractual arrangements, especially those with governments — commonly known as Service Concession Arrangements, the AASB has issued Interpretation 12 to address such contracts

- reviewing similar contracts with different customers varying between point-in-time and over-time revenue recognition, depending on specific contractual provisions

- differentiating in a contract between a ‘promise’ and a ‘performance obligation’

- differentiating in a contract between ‘milestones’ and ‘performance obligations’

- measuring variable consideration – especially where significant uncertainty exists.