Modern Australia has a vibrant knowledge economy. Highly skilled lawyers, accountants, engineers, architects, consultants and business managers contribute not only to our own economy but to the global one as well. However, professional services are often the intermediaries. They connect people to businesses, bring concepts to life and play pivotal supporting roles to our cities and the economy.

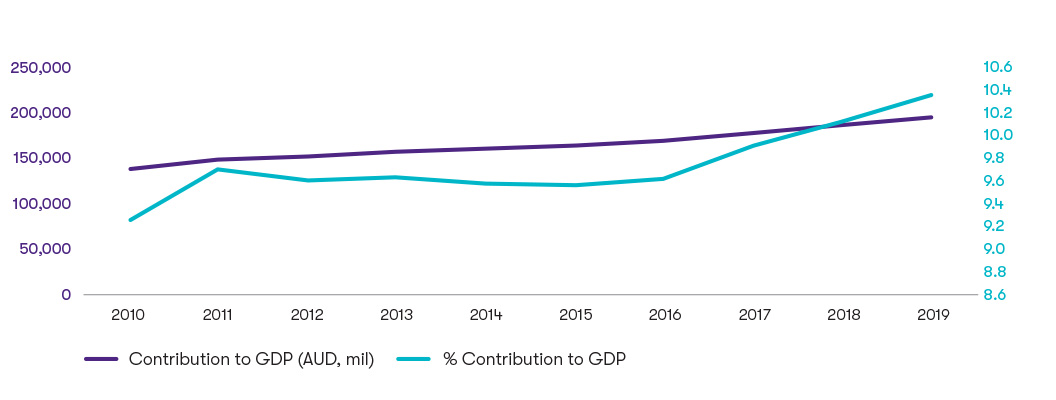

When you’re an intermediary you are far more likely to be subject to regulation rather than to benefit from direct funding. The Government really hasn’t invested much to support the sector in the last decade. However, professional services are indirect beneficiaries of funding to other parts of the economy, which would account for the strong contribution to GDP. Professional services has represented 10% or more of Australia’s GDP since 2017.![GTAL_2020_PS_FB_Graph.jpg]()

The contribution to GDP will no doubt grow as the sector supports the economy to grow out of recession

We know that integrity and compliance is just as, if not more, important when times are tough. Meeting employer obligations, as well as addressing more recent legislation around modern slavery will need to be balanced with incoming changes to Australian insolvency laws, tightening of the Foreign Investment Review Board and, of course, the new and significant investment in infrastructure, modern manufacturing, energy and digital. The opportunity now is to ensure the professional services sector is geared up with the right experts and connections to support clients, both existing and new, with the shift. The shift isn’t just in where Australia will focus their investments, it’s also closer to home in how we work. Now is the time to start positioning for that future.

In our report we cover:

- The indirect beneficiaries

- Professional services as valuable as ever

- Workforce changes

- So where to from here?

![GTAL_2020_Federal-Budget-2020-21.jpg]()

Looking back to look forward

We were initially writing the ‘Federal Budget: A 10 year retrospective’ report before COVID-19 as an advocacy piece for more industry investment and support. Of course, the way the year started is not the way the year is ending. Many sectors that had been left to their own devices are now key for our recovery. Sovereign capability. Jobs. Digital economy. Modern manufacturing. Renewable future. Deregulation. Innovation. These are the terms we will use as we settle into COVID-normal.

Our report looks retrospectively at 13 different industries, the investment made into them by Government and their contribution to GDP. This is then overlaid with the opportunity we see for industry in this new normal based on recent Government announcements.

Download report