Calculating the amount of damages as part of an economic loss claim is not necessarily a simple matter of adding up a series of lost profits. In many (but not necessarily all) cases, they must be discounted to their present value.

In this article, we will discuss some of the key considerations and challenges in applying discounting and discount rates in economic loss calculations.

What is discounting and why is it necessary?

Discounting is the process of expressing the value of a future cash flow (the losses) at a point in time, usually the date of the breach or event that caused the loss. A discount rate is applied to the future cash flow to calculate its present value, and reflects both the time value of money) and the risk of the future cash flow.

Discounting is necessary to:

- avoid overcompensating the plaintiff, who would receive a windfall if awarded the full amount of the future loss without discounting. For example, if $1m in profits was lost over five years and $1m was awarded today, the $1m could be invested and a return received. The plaintiff would gain in excess of $1m as a consequence of the award.

- Reflect the economic reality of the loss, which is directly linked to time. The value of the loss depends on when it occurs and how long it lasts. For example, a loss of $200,000 in year one is worth more than a loss of $200,000 in year five.

What are the key considerations in discounting?

There are three key considerations in discounting:

-

The date the loss is being discounted to, also known as the present value date. This may be the date of the breach or event, the date of the loss assessment or some future date (such as the expected court date), or no discounting at all. The choice of the present value date may depend on the legal principles, the availability of data, the purpose of the report, and the expert’s judgment.

-

The type of loss being discounted, which determines the type of discount rate. The discount rate needs to match the type of cash flow. For example, if the loss is measured on a pre-tax basis, the discount rate should also be pre-tax. If the loss is measured on an after-tax basis, the discount rate should also be after-tax. The result should be the same whichever is applied, as long as the discount rate is consistent with the cash flow.

-

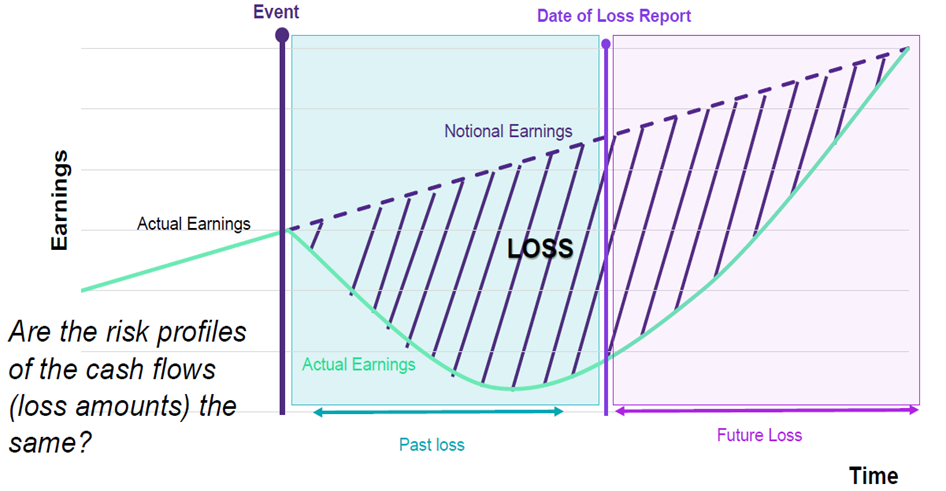

Different discount rates for past and future losses. This may be appropriate to reflect the different risk profiles of the cash flows. Past losses may be viewed as less risky because they are based on actual or historical data, rather than projections or assumptions. In a case where there were future losses attributable to a new business income stream, these would be more risky than future losses stemming from an established business income stream.

![]()

How to determine the appropriate discount rate

The appropriate discount rate is one that reflects the risk and return of the lost cash flow, or the opportunity cost of the plaintiff. Essentially, it is the rate that the plaintiff could have earned by investing the lost cash flow in a comparable project or asset.

One common approach to determine the discount rate is to use the cost of equity or the weighted average cost of capital (WACC) relevant to the nature of the loss. WACC is derived from the capital asset pricing model (CAPM). The cost of equity represents the compensation that the market demands in exchange for owning the asset and bearing the risk of ownership.

However, there are some challenges and limitations in applying the CAPM, such as:

- The subjectivity or reliability of the input data, such as the market risk premium, the beta, and the debt ratios of comparable companies, which may vary depending on the source, time period, and the market conditions.

- The assumption that the risk of the business’s cash flows is the same as the risk of the lost cash flows, which may not be true in some cases.

- The lack of transparency and consistency in the calculation and adjustments made to the discount rate, which may lead to disputes and confusion among the parties and the court. For example, some experts may apply a company-specific risk premium, a size premium, or a liquidity premium.

What are the potential pitfalls and best practices in discounting?

Discounting can be a complex and sometimes subjective process that requires careful analysis and judgment. Some issues to keep in mind include:

-

Avoid an over-simplification or generalisation of the discounting process, such as applying a single or arbitrary discount rate to the entire loss. The discounting process should be tailored to the specific facts and circumstances of the case.

-

Avoid double-counting or double-dipping of the discounting factors. This is often seen when a matter is reflected in both the discount rate and to the cash flow itself.

-

Communicating and presenting the discounting process and results clearly and concisely can be difficult in complex calculations. However, it is vital to understand all the inputs and calculations.

Conclusion

Discounting and discount rates are important and challenging aspects of economic loss calculations. As forensic accountants and expert witnesses, we have the skills and experience to assist our clients and the court in applying discounting and discount rates in a sound and reasonable manner, and to provide clear and compelling evidence and evidence on the quantum of damages.

Learn more about how our Forensics services can help you