The last few years have by and large been spent tightening the taxation screws on property investors in an attempt to deal with the housing affordability issue – but it has been a blanket approach.

While some cities had the highest occupancy rates in years and property prices that were off the charts, other regions had stagnated and saw little growth in prices. Things had started to cool as a result of the measures, in conjunction with restrictions introduced for foreign buyers - and now COVID-19 has thrown up a whole new round of challenges.

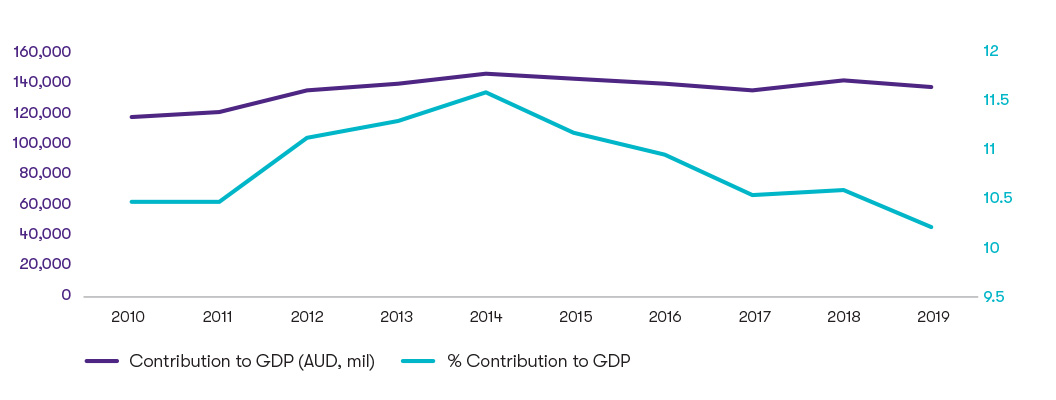

The Budget and Expenditure data in our ‘Federal Budget: A 10 year retrospective’ is representative of infrastructure spend. The data demonstrates a bumpy ride but real estate & construction has been the highest contributor to Australia’s GDP over the last 10 years, sitting at an average of 10.85%.

While the dollar value of contribution has remained relatively steady in these years, the sector’s percentage contribution to Australia’s GDP has dropped – largely due to booms in other sectors such as resources. Getting the balance right for housing supply and demand has always been the challenge, and infrastructure investment in our cities has seen years of expenditure followed by years of regulation to contain the market, and around we go again.![GTAL_2020_REC_FB_Graph.jpg]()

Activation through infrastructure

It’s widely known that the real estate & construction industry is a key engine for our economy. The Federal Government brought forward a significant amount of funding to put more “boots and utes” on the ground. However, infrastructure is much more than just roads and bridges and Australia needs to redesign it’s messaging around infrastructure funding. To keep construction firms and services that feed into them operating, we also need built form infrastructure to assist the expansion of communities and regions. With net migration down for the foreseeable future, and more people moving to regional areas, do we need to rethink where these investments are made? Certainly the impressive investment in upgrades to the NBN to close the digital divide between urban and regional Australia suggests that the Government is seeing opportunity outside of our major city centres.

In our report we cover:

- Did Australian property overshoot?

- The impact of stalling net migration

- Do we need a foreign investment revival?

- Activation through infrastructure

- Unlocking the regions

- So where to from here?

![GTAL_2020_Federal-Budget-2020-21.jpg]()

Looking back to look forward

We were initially writing the ‘Federal Budget: A 10 year retrospective’ report before COVID-19 as an advocacy piece for more industry investment and support. Of course, the way the year started is not the way the year is ending. Many sectors that had been left to their own devices are now key for our recovery. Sovereign capability. Jobs. Digital economy. Modern manufacturing. Renewable future. Deregulation. Innovation. These are the terms we will use as we settle into COVID-normal.

Our report looks retrospectively at 13 different industries, the investment made into them by Government and their contribution to GDP. This is then overlaid with the opportunity we see for industry in this new normal based on recent Government announcements.

Download report