Employee fraud can be perpetrated through the misappropriation of assets and/or financial statement misstatement.

The Association of Certified Fraud Examiners (ACFE) in their 2023 Global Fraud Survey identified that in the period between January 2022 and September 2023, 89 per cent of fraud cases involved the misappropriation of assets, with a median loss of USD $120,000 per case.

While financial statement misstatement accounted for 5 per cent of fraud cases, the median loss per case was significantly higher at USD $766,000 per case.

Employee fraud can take some time to be detected, so awareness is key.

Who’s responsible for the prevention and detection of employee fraud?

In the first instance, the responsibility of prevention and detection of fraud rests with management and those charged with governance.

In their executive day-to-day function in the business, management have a responsibility to prevent, reduce opportunities and deter fraud from taking place.

Those charged with governance are responsible for the oversight of management. There exists an inherent fraud risk within management’s ability to override internal controls.

More broadly, all employees have a responsibility to prevent and detect fraud. In the same ACFE survey, of all fraud detected, more than half were reported by employees.

Fraud risk has been on the rise since the COVID-19 pandemic, so what are the risk factors that management and those charged with governance can look out for?

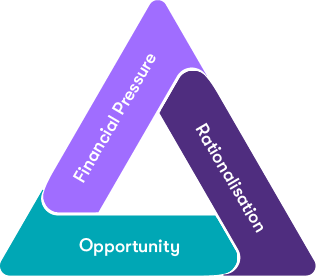

Fraud triangle

The fraud triangle highlights the three characteristics (incentive, opportunity and rationalisation) that can lead to instances of employee fraud.

Risk factors to look out for

We’ve detailed some common employee fraud risk factors we see under each characteristic of the fraud triangle.

Challenging personal financial obligations of employees.

Adverse relationships between the employer and employees.

Large amounts of cash on hand or processed.

Inventory and fixed assets that are small in size, of high value, in high demand and easily convertible to cash.

Inadequate segregation of duties or independent checks.

Inadequate oversight of senior management expenditures e.g. travel reimbursements.

Inadequate job applicant screening of employees with access to assets.

Lack of complete and timely reconciliations of assets.

Lack of timely and appropriate documentation of transactions e.g. merchandise returns.

Lack of mandatory holidays for employees performing key control functions.

Inadequate management understanding of information technology, which enables information technology employees to perpetrate a misappropriation.

Disregard for internal controls.

Failing to take appropriate remedial action on known internal control deficiencies.

Behaviour indicating displeasure with employer.

Changes in behaviour or lifestyle.

Tolerance of petty theft.

We’re here to help

By implementing controls to address the employee fraud risk factors, organisations can protect themselves from financial loss. If need assistance with your processes and want to ensure you’re not vulnerable to fraudulent activity, please don't hesitate to reach out to our team of specialists today.

Learn more about how our Forensics services can help you

Accounts payable and payroll fraud conducted by employees is an issue that can have a negative impact on businesses. Detecting and investigating these types of fraud requires a systematic approach to identify irregularities, gather evidence, and take appropriate action against the perpetrators.

Workplace fraud is a serious and costly issue that can impact organisations across different sectors and regions – and is becoming increasingly relevant as cost-of-living pressures rise.

To minimise the impact of fraud in Australia and globally, we are promoting anti-fraud awareness and education with a series of articles during International Fraud Awareness Week. This article is the first in our series and takes a closer look at the most commonly experienced types of fraud, the warning signs, and fraud detection.

Subscribe now to be kept up-to-date with timely and relevant insights, unique to the nature of your business, your areas of interest and the industry in which you operate.