As discussed in our earlier article, this type of fraud refers to any dishonest or illegal activity committed by an employee or a group of employees for personal benefit, appearing in various forms, such as theft, corruption, bribery, falsification of records, and the misuse and misappropriation of assets.

The Association of Certified Fraud Examiners (ACFE) estimated in the 2022 Report to the Nations1 that workplace related fraud had cost organisations $4.7 trillion globally, with the median loss of each case accounting for approximately $117,000. The ACFE outlined that the most common control weaknesses contributing toward the enablement of this type of fraud included:

The reason why workplace fraud is so prevalent is due to two key factors: trust and opportunity. Entrusting employees with access to controls and assets is critical for an organisation to function effectively. Through this trust, as well as opportunity through an employee’s role or position, the risk of workplace fraud poses a major threat to businesses of all sizes and types. As such, it is critical that organisations understand this risk, how to identify the red flags, and adopt fit for purpose controls to best mitigate this threat.

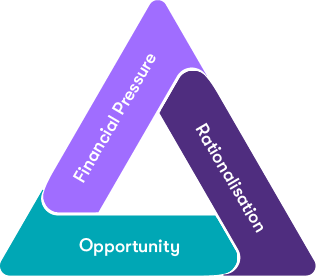

Understanding the fraud triangle

To understand the causes and consequences of fraud, organisations can use the Fraud Triangle, a theoretical framework that identifies the primary factors influencing fraudulent behaviour.

The three key elements responsible for fraud include:

- Pressure

- Rationalisation

- Opportunity

![]()

You can read more about the fraud triangle in our previous alert.

While the fraud triangle suggests fraud is more likely to occur when all three elements are present, given the current scenario where both external pressure and rationalisation coexist, it is more important than ever for organisations to have effective and fit for purpose mitigants of fraud – or reduce the ‘opportunity’ – as much as possible.

Internal Audit’s Role in Fraud Mitigation

As found by the ACFE, a lack of internal controls and the overriding of existing controls were the primary enablers of workplace fraud. An Internal Audit is a valuable tool that organisations can use to conduct a comprehensive fraud assessment throughout the entire company, assessing the existence and design of organisational controls, as well as how effective adopted controls work in practice. This proactive oversight allows for the early detection of red flags, inconsistencies, and irregularities that might assist in indicating fraudulent activities.

By conducting these risk assessments, a robust internal audit program can assist in identifying areas most susceptible to fraud, enabling the implementation of targeted preventive measures to deter and prevent fraud.

Contact us for more information on conducting an internal audit today.

[1] ACFE: Occupational Fraud – Report to the Nations 2022 2022+Report+to+the+Nations.pdf (amazonaws.com)

Learn more about how our Internal audit services can help you