Four financial trends for Higher Education in 2020

23 Jan 2020The Australian higher education sector has been going through a period of rapid change.

This includes new technologies, changes to student demographics and the way that people prefer to learn, changes to what employers are looking for from graduates, and changes to the way that universities are funded (just to name a few). Amongst this ongoing change, it is useful to step back from time to time and have a look at what’s happening in the sector.

Here are some interesting macro trends that we have noticed from our recent financial analysis of the public higher education sector.

-

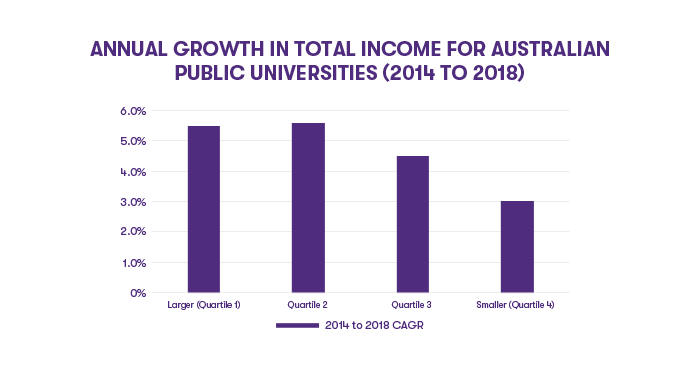

Our smaller universities are growing at a much slower pace than our larger universities.

Our larger universities (top quartile for income in 2014) have grown by 5.5% p/a over the last 5 years (CAGR). Our smaller universities (bottom quartile in 2014) have grown by 3% p/a over the same period.

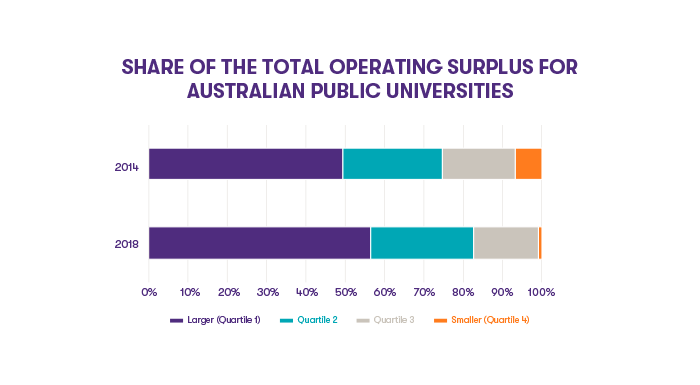

In 2014 the top quartile (by income) generated 49% of the sector’s operating surplus, and the bottom quartile generated 7%. By 2018 this disparity has increased, and is now 57% versus 1%.

If this trend continues it will mean that the smaller universities, including those based in regional centres, may find it harder to compete with the financial resources of larger universities.

-

Expenses are growing faster than income.

Across the public higher education sector, expenses increased by 5.9% p/a from 2014 to 2018, while income increased by only 5.1% p/a. Correlating with this, the sector's total operating surplus in 2018 was 24% less than in 2014.

If this trend continues there is obviously a point where expenses will be higher than income, and for some universities, this is a more present issue than for others. Some smaller universities, in particular, are already reporting operating deficits more frequently.

Short term operating surplus isn’t everything – particularly in the public education sector, where other outcomes (such as student success and research outcomes) are a driving force. But operating surplus can be an indication of the capacity to invest in the future, and each university needs to find a way to be financially sustainable over the long term.

-

International students have become increasingly important.

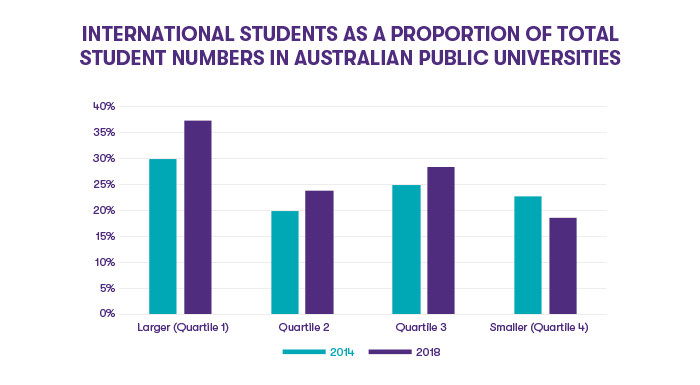

With per-student funding for domestic students having largely flatlined, many universities have increased their focus on international student numbers. International student numbers have grown, and now makeup 30% of total students across the sector. This growth has been disparate. For larger (top quartile income) universities, international student numbers have grown to be 37% of their students, while for smaller (bottom quartile income) universities this has decreased to 19%.

Conditions have been relatively favourable for attracting and retaining international students over recent times (such as visa regulations, the Australian dollar, global economic conditions, international relationships, and a growing middle class in several target markets). However, these conditions can turn around quickly, and universities who over-rely on international students will need to have a course of action for dealing with any drop-off in demand.

Similarly, universities who are overly reliant on any single market for their international students may find themselves exposed in the event that the external environment changes.

-

The sector continues to invest in the future.

While the accounting treatment of some investments makes it challenging to draw solid conclusions from balance sheets, it is interesting to note that the total assets of the public higher education sector have grown by 5.5% p/a from 2014 to 2018 (CAGR). This indicates that as a sector, investment in assets has outpaced depreciation by a significant amount.

Part of this may be attributable to the time value of money, but even so, this is a positive sign for the future capacity of our higher education sector.