These new standards have been implemented to improve alignment with the Australian Prudential Regulatory Authority (APRA)’s insurance capital framework, consistent with international best practice.

The new capital framework for life insurance, general insurance, and public health insurance companies came into effect with the aim of further strengthening financial resilience across the sector.

As many PHIs are undergoing major changes not only brought about by the new PHI capital framework, but the new accounting standard AASB 17 Insurance Contracts (AASB 17), this challenge is leaving room for further improvement to uplift industry better practice and enhance capital management and oversight.

For insurers, embracing these tangible changes is not just a regulatory necessity but a strategic imperative in navigating the evolving landscape of financial resilience.

The capital framework aims to provide standard guidance on how to measure capital requirement that will support overall financial resilience against unforeseen headwinds.

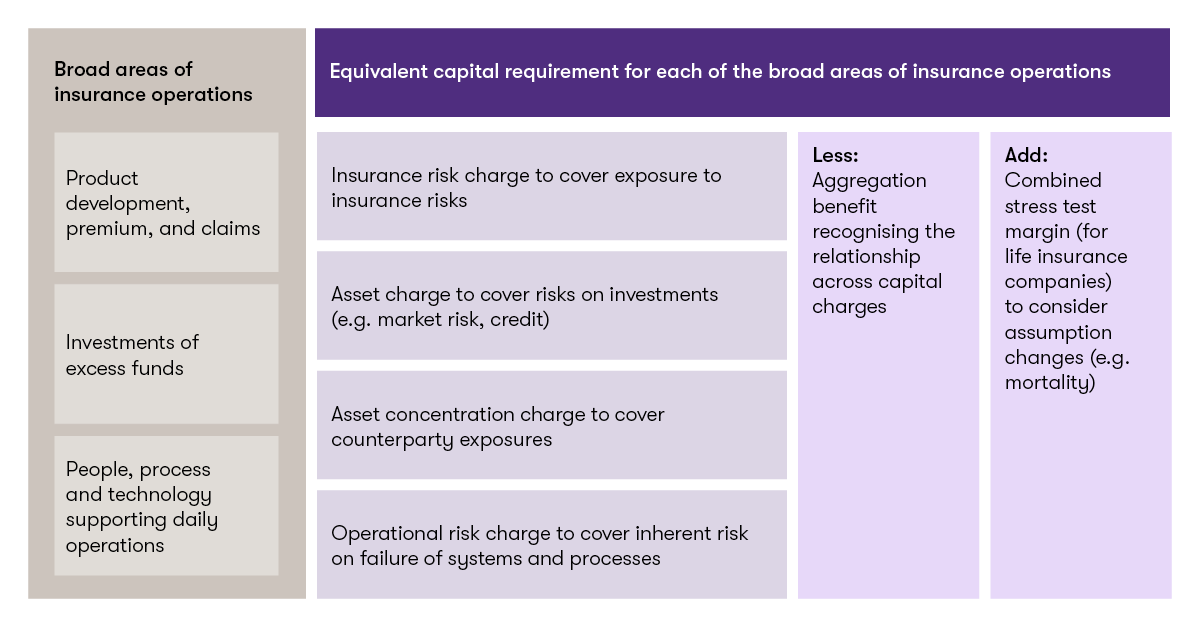

Key Requirements for all insurers

The new capital framework requires all insurers to calculate their prudential capital requirements based on the new guidance and formula for each of the equivalent capital charge. While the calculation may involve some complex mathematical calculations, each of the capital charges can be mapped to the broad areas of insurance operations and relating them to the various risks that an insurer is exposed to.

![]()

While the revised capital framework provides some level of standardised calculations for the prudential capital requirement (PCR), the key focus area of the revised capital framework is to provide better understanding of how the current business strategy affects the insurers’ risk exposures and its impact on capital.

As part of its supervisory function, APRA can prescribe other amounts of PCR if the outcome of the standardised calculations are deemed not reflective of an insurer’s exposure.

The capital framework beyond regulatory compliance

Beyond regulatory compliance, the application of the new capital framework enables:

1. Understanding of risk exposures and its impact on capital

The new capital framework provides for a standardised method that can enhance an insurers’ understanding of its risk exposures arising from products offered (including claims history), investments held, and the processes performed.

2. Enhanced comparability across insurance sector

While products offered may vary from insurer to insurer, the application of the new capital framework will enable more consistent reporting of capital charge enhancing comparability across periods and between entities.

3. Improved oversight by those charged with governance

With a more consistent reporting of capital charge for each of the risks identified in the new capital framework, the Board can have better understanding of the linkage between its operations and capital requirements. With this better understanding, the Board can provide better oversight helping the future sustainability of an insurer’s operations.

4. More mature internal capital adequacy assessment process

With capital serving as a buffer for unforeseen losses and supporting future growth, appropriate capital planning is a key focus area in the sector. The new capital framework further requires more mature capital planning with the processes being actively embedded in the business. Insurers are expected to consider various severe, yet plausible, stress scenarios and assess its impact on future capital requirements.

We’re here to help

Organisations seeking further insights into how the new capital framework impacts their business are encouraged to reach out for guidance to ensure compliance with the forthcoming standards.

Learn more about our Financial Services team