We have undertaken a significant number of ESIC reviews for companies both under the principles-based test and the 100-point test. Some of our key findings to date are as follows:

The ATO is well aware that some companies implement contrived ‘schemes’ designed to enable them to be an eligible ESIC.

The ATO is keen to engage proactively with companies to determine their eligibility, particularly when companies engage under the PBR program.

Investors are demanding evidence from ESICs about how they have determined their eligibility.

The ATO views the ESIC measures as strictly applicable for companies ‘developing’ new or improved products, processes or, services and is alert to companies that have already developed their product, process or service.

Depending on your specific circumstances, we offer two options to help a company determine if they are an ESIC:

Review option We can provide you a tailored template to assist with your documentation for support (generally a PBR application), review the document and manage correspondence with the ATO where required; or

Preparation option We draft the support document, liaise with the ATO (where required) and submit the PBR on your behalf (where required).

Although tech-enabled businesses are increasingly attractive for investors, many Early Stage Innovation Companies (ESICs) face stiff competition for investor capital.

Contents

That’s why the Australian Government’s ESIC measures to incentivise investment in these companies are key to supporting the Federal Government’s sovereign manufacturing innovation agenda.

Why is the ESIC regime so attractive?

The ESIC regime provides tax incentives to investors who acquire shares directly from ESICs, assisting in the funding of those companies.

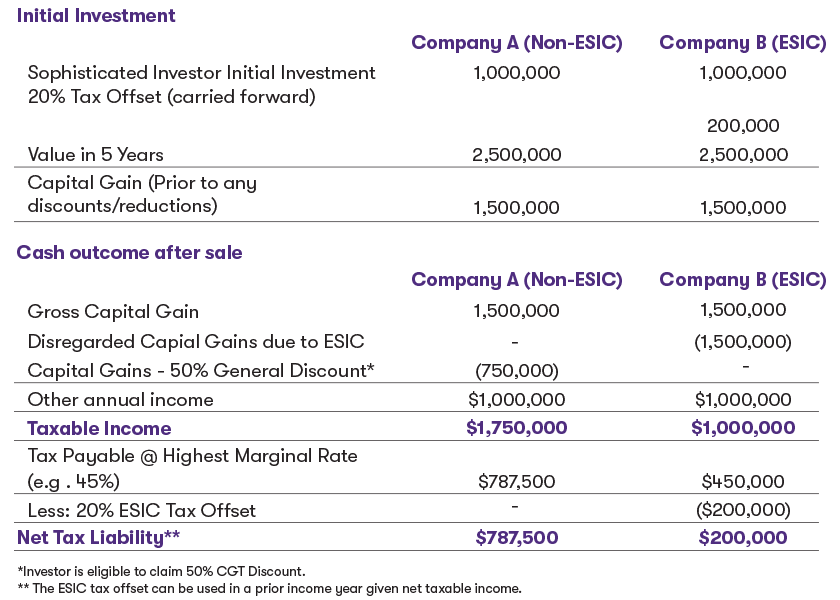

Tax offset: The investor will be eligible for a tax offset calculated based on 20 per cent of the investor’s investment in the ESIC and is capped at $200,000 for “sophisticated investors” and $10,000 for “non-sophisticated investors”.

CGT exemption: Where the shares have been continuously held for at least 12 months and less than 10 years, any CGT gain or loss will also be disregarded for tax purposes. For ESIC shares that are held for a period greater than 10 years, an uplift in the tax cost base of the shares to the market value of the shares 10 years after acquisition.

Is your company ESIC eligible?

To be an eligible, your company broadly needs to be an innovative company in its early stages with high-growth potential, a geographically broad offering and the ability to scale-up.

The tests to determine this are:

This test identifies whether or not a company is in its ‘early stages’. This is evidenced by a company’s previous year’s income and expenses, along with its date of incorporation or registration. The criteria can be found here.

100-point test (objective) – To pass the 100-point test, a company is required to accumulate at least 100 points based on specific criteria determined to be indicative of an innovative company. Refer to this table provided by the ATO to determine whether your company is able to satisfy the specific criteria and accumulate at least 100-points; or

Principles-based test (subjective) – This test identifies if a company is developing a new or significantly improved innovation (product, process, service) to be commercialised (i.e. to generate income) and has high-growth potential with the ability to scale across a broad market. Due to the subjectivity in applying this test, it is good practice (and our recommendation) to obtain a Private Binding Ruling (PBR) from the ATO to confirm eligibility.

Gaining certainty through a private binding ruling (PBR)

In order to obtain the above concession, we encourage your company to obtain a private binding ruling (PBR) from the ATO, confirming that the company is an ESIC company.

Research and Development Tax Incentive

Depending on the route taken with regards to the ESIC tests, the information included as a part of an ESIC Application can often be a great starting point to consider leveraging the R&D Tax Incentive (RDTI). The program provides targeted R&D tax offsets designed to encourage companies to engage in R&D in Australia.

The RDTI has different levels of support depending on a company’s aggregated turnover (grouping rules apply):

Where turnover is below $20m, offsets are refundable and equal to the company’s corporate tax rate plus an 18.5 per cent premium on eligible expenditure. In some cases, this could result in a cash refund from the ATO.

Where turnover is above $20m, the offset is non-refundable but can be carried forward to offset future income tax obligations. The offset rate is equal to the company’s corporate tax rate plus 8.5 per cent, but may be up to 16.5 per cent depending on the R&D intensity for the income year. The higher rate is available to companies that achieve an R&D intensity (spend) of greater than 2 per cent of their total expenses.

The RDTI is a self-assessment program. It’s crucial that any RDTI claim comprises robust governance processes and substantiating documentation.

Given the time pressures and the administrative burdens, please reach out to discuss your eligibility for these tax concessions and innovation incentives. Our experts will be able to assess your eligibility for these significant concessions and help you navigate the requirements.

Learn more about how our Research and Development (R&D) Tax Incentive services can help you

In this edition of our Australian International Tax Update, we summarise recent significant Australian tax developments, examine their practical impact, and outline actions that multinational groups, foreign investors, private equity funds and international advisers should consider.

Following the release of Exposure Draft legislation on 10 April 2026, on 2 July 2026 the Government introduced the Treasury Laws Amendment (Strengthening Accountability for Tax Adviser Misconduct and Other Measures) Bill 2026 into Parliament.

FY26 was a defining year for Australia's Research and Development Tax Incentive (RDTI), and for the wider conversation about how Australia funds innovation.

Subscribe now to be kept up-to-date with timely and relevant insights, unique to the nature of your business, your areas of interest and the industry in which you operate.