One area that demands particular attention is the family trust election (FTE). While FTEs can unlock valuable tax concessions, they also carry significant compliance risks. A misstep can trigger the family trust distributions tax (FTDT), which is levied at the top marginal tax rate plus the Medicare levy, currently totalling 47%.

What is an FTE, and why is it relevant?

A family trust can access a range of tax concessions, including the ability to pass on franking credits to beneficiaries and more easily deduct carried-forward tax losses in trusts and companies. A trust (particularly a non-fixed trust which incorporates both family discretionary trusts and most hybrid trusts) becomes a family trust at any time when a valid family trust election in respect of the trust is in force. A valid FTE would require nominating someone as a ‘test individual’. However, this comes with important limitations. Once a trust becomes a family trust, it can only make distributions within the ‘family group’ of the test individual without triggering FTDT. The definition of the family group includes the test individual’s spouse, any parent or grandparent, siblings, etc. Certain entities such as companies, other trusts, and partnerships can also be included in the family group, provided other members of the family group hold fixed interests in them or make a valid FTE or interposed entity election (IEE), which requires passing something called the family control test (discussed in this article). While the definition of the family group appears broad, in practice, having an FTE or IEE in place can make business operations quite restrictive. For example, having an IEE in place for a company could make the sale of shares to someone outside the family group impossible without triggering FTDT. Therefore, FTEs or IEEs should only be made after careful consideration of all implications.

A scenario where FTDT can arise

Let us take a look at a scenario of when FTDT can arise when new trust beneficiary companies are established that are owned by different new trusts to facilitate succession planning.

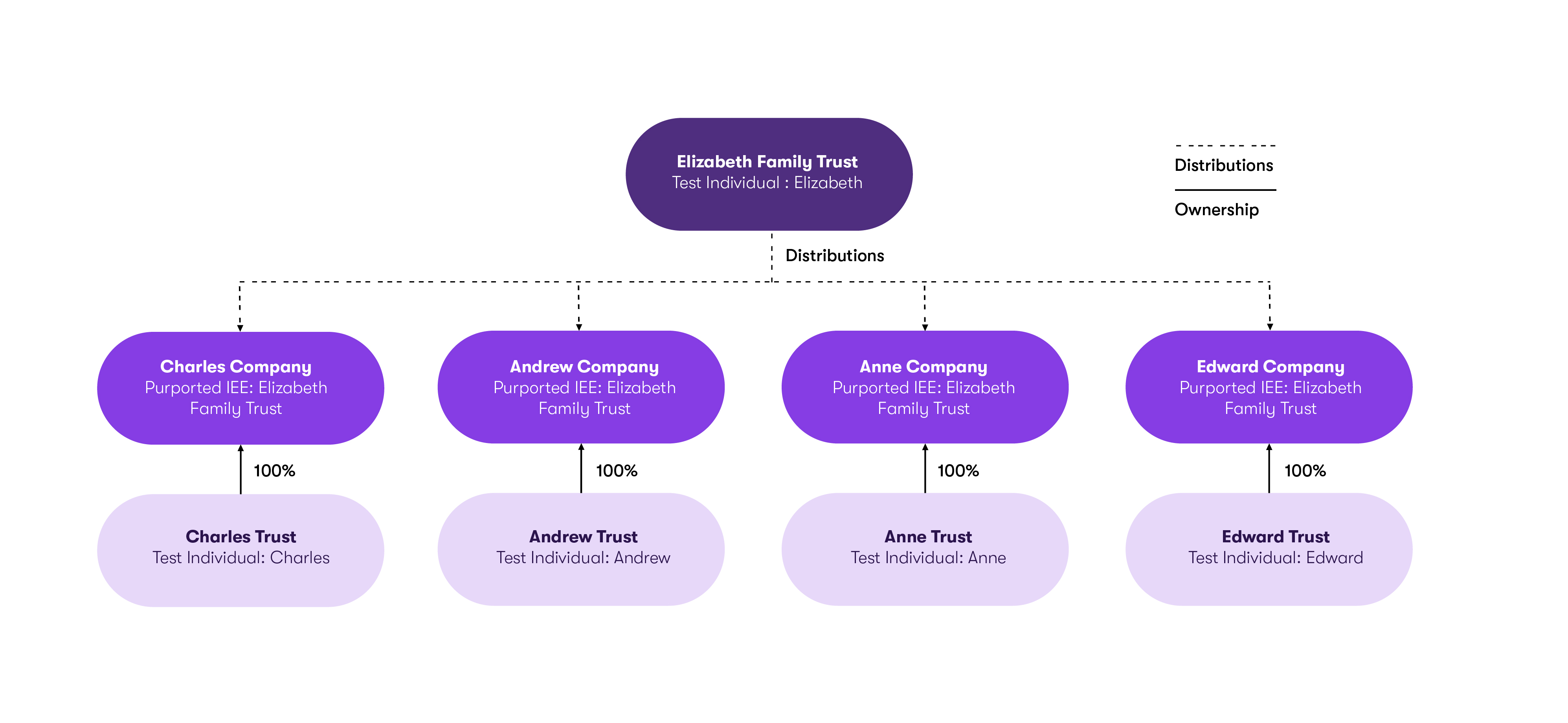

The Elizabeth Family Group

The assets of the Elizabeth Family Group are owned and controlled by Liz Pty Limited as trustee for the Elizabeth Family Trust. An FTE for the Elizabeth Family Trust commenced on 1 January 2000, with Elizabeth nominated as the test individual. Elizabeth passed away on 12 April 2018, leaving four adult children: Charles, Andrew, Anne, and Edward. These children, along with their controlled entities, are beneficiaries of the Elizabeth Family Trust. Between Elizabeth’s death and 30 June 2022, each of the four children incorporated Australian resident companies (beneficiary companies). The beneficiary companies are wholly owned by the children’s respective Australian resident trusts (beneficiary trusts). The beneficiary companies each purported to make IEEs in favour of the Elizabeth Family Trust. The beneficiary trusts have made FTEs in favour of the respective children. A number of distributions were made from the Elizabeth Family Trust to the beneficiary companies from 2018–2022 (see Figure 1).

![]()

View diagram

What are the arising issues?

This scenario highlights several compliance risks. The Elizabeth Family Trust made an FTE with Elizabeth as the specified test individual. This means that all trust distributions from the Elizabeth Family Trust must be made to individuals or entities within Elizabeth’s family group. Distributions to beneficiaries outside of the family group will trigger FTDT. Each of the beneficiary trusts has made FTEs in favour of each of the respective children and, therefore, sit outside of Elizabeth’s family group. In attempting to rectify this, each of the beneficiary companies purported to make IEEs in favour of Elizabeth. However, to be valid, they need to pass the family control test. The family control test is failed by each beneficiary company for the following reasons:

- The individual specified in the FTEs of each of the beneficiary trusts is not Elizabeth. Therefore, the beneficiary trusts are not part of Elizabeth’s family group.

- Members of Elizabeth’s family group have less than 50% of fixed entitlements to income and capital of the beneficiary companies. The fixed entitlements are taken to sit with the beneficiary trusts, which own 100%.

- This would be remedied if members of Elizabeth’s family group held fixed entitlements in each of the beneficiary trusts, but they are discretionary/non-fixed trusts.

As the family control test is failed, the IEEs are not valid, and the beneficiary companies are not in Elizabeth’s family group. FTDT will apply to distributions made by the Elizabeth Family Trust to the beneficiary companies from 2018–2022. FTDT is generally due and payable 21 days after the date of distribution. As the FTDT liability has been discovered and thus paid late, general interest charges (GIC) may also apply.

When the FTDT is paid, the beneficiary companies will be able to claim refunds for previous corporate tax paid on distributions received. However, this will lead to further tax inefficiency as the companies will hold increased retained earnings but no franking credits to reduce the tax payable. The resulting overall outcome could be an effective tax rate of 94% plus interest.

What should have happened?

If the assets of the Elizabeth Family Trust were to be kept together, the focus should have been on ensuring distributions were made within Elizabeth’s family group. Due to the many non-tax issues that affect families and wealth held in private groups, solutions to this dilemma might not be available, but may include:

- establishing entities earlier than when needed, which may improve the ability to add them to desired family groups

- otherwise, to focus more carefully on the structure of the new companies so that FTDT may be avoided if they receive trust distributions.

What steps are suggested to fix the issue?

The Elizabeth family group can consider taking following steps to fix the issue:

- Although the trustee is legally required to pay Family Trust Distributions Tax (FTDT), the amount received by the beneficiary is treated as non‑assessable, non‑exempt income, i.e. non-taxable. In some cases, this can result in a tax‑neutral outcome. However, this is not always the case. For example, adverse outcomes can arise where the distribution relates to fully franked dividends, discounted capital gains, or is made to a company. As a result, the first practical step is to assess the overall tax and cash flow impact of FTDT across the group. This typically involves a multi‑year review of how distributions have flowed between trusts, companies and individuals, whether distributions remain frankable, the effect on franking credit balances, how the FTDT will be funded, and the overall effective tax cost to the group.

- The ATO is currently offering interest relief until 31 December 2026 for family trusts that have unintentionally distributed income outside their family group, triggering FTDT. Where taxpayers proactively review their position, make a voluntary disclosure and pay the FTDT by this date, the ATO may remit up to 80 per cent of any general interest charge. This can materially reduce the overall cash outlay. Based on the outcome of the impact assessment above, it would be prudent for the trustee of the Elizabeth Family Trust to make a voluntary disclosure to the ATO and pay the FTDT to prevent further interest accruing. Once the ATO confirms the position, relevant members of the Elizabeth group may then need to lodge amended tax returns.

- Given the potentially significant impact on cash flow and franking credit balances, it is important to put appropriate tax governance processes in place to reduce the risk of similar issues arising in the future, including unintended FTDT exposures. A well‑designed tax governance framework can help ensure that the tax implications of future distributions are considered before they are made. Importantly, effective tax governance does not need to be complex. It should be proportionate to the size and complexity of the business and focus on clear roles, accountability and consistent decision‑making.

Proactive risk management: What are the key triggers of FTDT?

The risk of FTDT can significantly increase in the following situations:

- An FTE or IEE has been put in place by a current or previous adviser, and you are unaware of its implications. Thus, you might trigger FTDT liability without realising it. We recommend a detailed assessment to understand the benefits, consequences, and pitfalls.

- The family has grown or changed since the original FTE was made, resulting in beneficiaries who are not part of the family group. A structure review is advisable to ensure it remains fit for purpose and to be aware of who is included in the family group, so that FTDT can be avoided.

- A business restructure has occurred, and an entity is no longer controlled by the family group. A review should be undertaken to assess the impact and determine if the entity can be brought back within the family group.

- The tax affairs of family members are managed independently by separate accountants, potentially resulting in mismatched distributions, FTEs and IEEs. If consolidation under one firm is not possible, an annual meeting between family members and their accountants is recommended.

- Death in the family, especially of a key founding member/test individual. The impact should be assessed as part of estate planning, as elections can only be made while that person is alive. It is also important to evaluate the requirement of FTE where the estate plan includes the establishment of testamentary trusts.

- There is a family breakup. Both parties should obtain independent advice, especially here a trust holds assets.

- A future sale of shares in a company with an IEE in place is planned. Careful review and planning are needed to ensure the election does not become an impediment.

- There is a potential Australian Taxation Office (ATO) review. If your group is likely to fall within the medium, large or emerging privately owned and wealthy category, there is a strong likelihood that the ATO will conduct a review of your tax affairs. We strongly recommend conducting a prudential review in advance to ensure readiness for any ATO engagement.

Conclusion

FTEs and IEEs can unlock tax benefits but must be carefully managed, as distributions outside the designated family group trigger FTDT at 47%. Complex family structures, succession planning, and changes such as death, divorce, or business restructuring can unintentionally breach FTE or IEE rules, leading to significant FTDT liabilities.

Proactive risk management, including early entity setup, regular structure reviews, and coordinated tax advice is essential to avoid costly FTDT consequences and ensure compliance.

Families should review their circumstances soon so that any matters of risk can be dealt with by 31 December 2026, while the current opportunity to obtain interest relief is available.

Article contributed to by Karen Tran - Private Business Tax & Advisory