This change is intended to account for changes in the Top 1000’s tax profiles, since this group was first created in 2016 when the ATO’s insights from CARs conducted. It’s essential that applicable Top 1000 taxpayers now consider how this revised approach may affect their tax risks and how they prepare for CARs.

The original ATO approach

Introduced in 2020, Combined Assurance Reviews are conducted on the Top 1000 taxpayer population. A Combined Assurance Review examines the targeted taxpayer’s activities over a four review period from an income tax and GST perspective, through detailed inquiries framed to cover the ATO’s four key areas of Justified Trust, namely:

- understanding a taxpayer’s tax governance framework

- identifying tax risks flagged to the market

- understanding significant and new transactions

- understanding why accounting and tax results vary.

The revised ATO approach

According to the ATO, there has been a significant increase in taxpayers now captured in the Top 1000 population due to a rise in companies exceeding the $250m turnover threshold, plus an increase in the number of taxpayers achieving and maintaining strong CAR outcomes (i.e. a Stage 2 tax governance and overall high assurance ratings). To ensure the ATO’s resources are best tailored to manage this now greater number of taxpayers within this demographic, as well as respond to the positive actions taken by companies to improve their tax governance processes, the ATO’s revised CAR approach to the Top 1000 population has the following key changes:

- The turnover threshold for applicable Top 1000 companies is now $350m (instead of $250m).

- The resulting Top 1000 population has been subdivided into two categories from an income tax perspective – ‘significant taxpayers’ and ‘general pool taxpayers’. The ATO will tailor the scope and nature of its CAR inquiries in the four-year review period, based on these new Top 1000 subcategories and the affected taxpayer’s previous CAR outcomes.

- From a GST perspective, taxpayers who achieved a stage 2 or 3 governance rating and medium or high assurance rating, in their next CAR the ATO will:

- Focus on GST governance improvements and actions taken to address concerns as noted in the last review.

- Use the GST Analytical tool to understand variances in accounting and GST reporting.

These changes are summarised as follows:

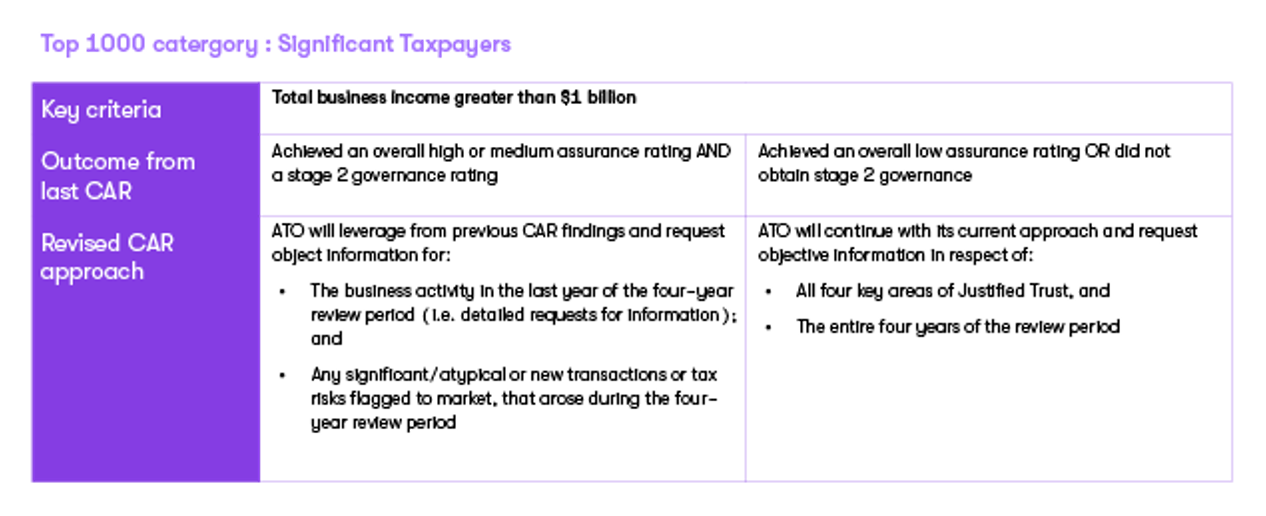

Top 1000 category: Significant Taxpayers

![]()

Expand table

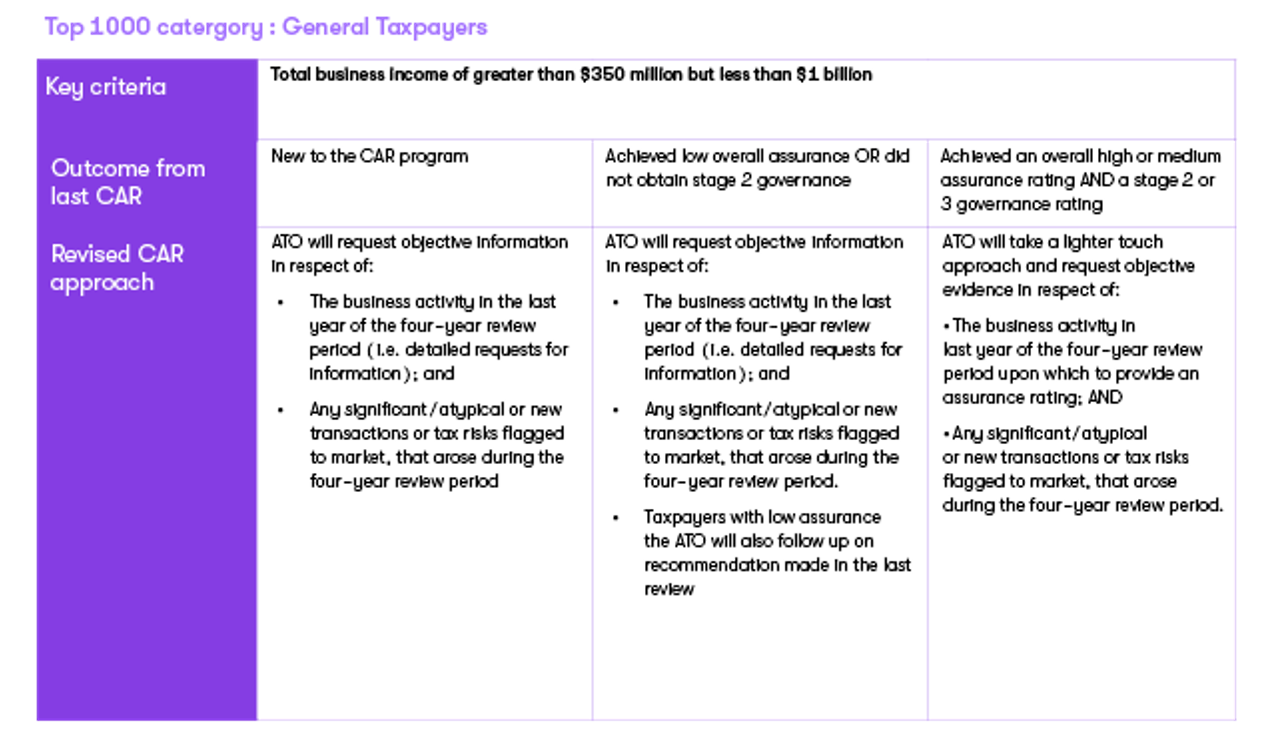

Top 1000 category: General Pool Taxpayers

![]()

Expand table

In practical terms, it’s clear the ATO is focused on tailoring their approach and resources on taxpayers who have stronger indicators of tax risk i.e. those with low assurance ratings or whose tax governance frameworks do not have objective evidence of improvement over time. The new $350m total business income threshold for Top 1000 candidates may grant a small reprieve to companies about to breach the previous $250m turnover threshold, but this shouldn’t materially change how these companies approach and document their tax risks and processes nor prepare for future CAR activity.

It's important to remember that the ATO still has a myriad of review programs it can deploy, outside its most well-publicised ones like the CAR refer to our earlier comments, to target taxpayers like those in this $250m to $350m turnover population for reviews of specific tax issues instead.

As the Top 1000 demographic knows, a CAR can take up substantial resources and costs to the organisation given the detailed nature of the CAR information request under the key areas of Justified Trust and four-year period under investigation. The fact that the ATO has now expressly stated their intention that a strong CAR outcome can limit the extent of inquiries in the next CAR, should be a strong motivator for taxpayers to take serious action to address its past CAR findings.

Our experience with all aspects of the tax governance process, means we’re well placed to help you work out where your organisation should focus to achieve your best outcome, and provide tailored solutions that suit your needs.

Contact us today and see how we can help.

Learn more about how our Tax services can help you