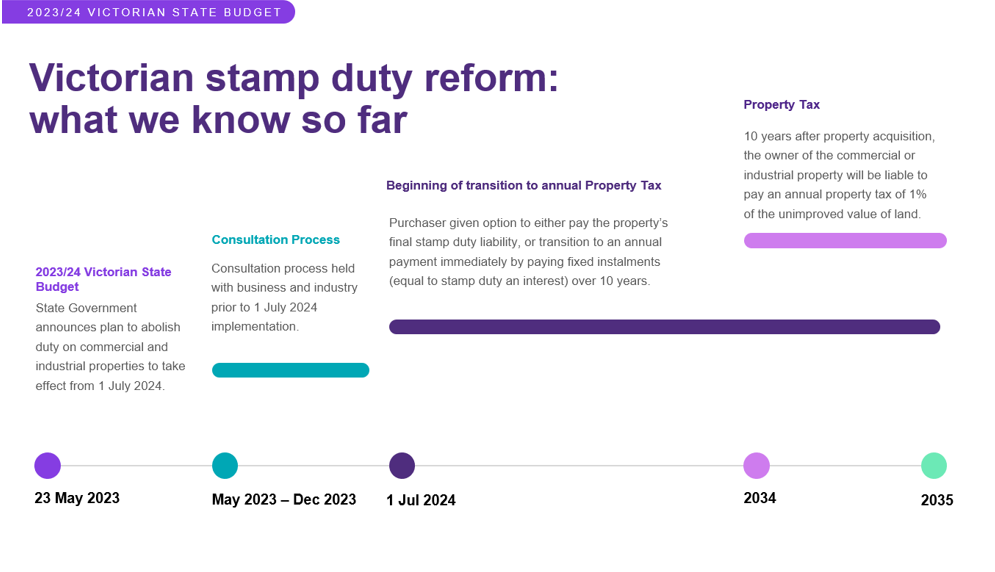

Abolition of stamp duty on commercial and industrial properties – what we know so far

The Government has announced that it plans to abolish stamp duty for commercial and industrial properties.

From 1 July 2024, commercial and industrial properties will transition to a new annual property tax system as they are sold. Although no draft legislation has been released, the limited information provided by the State Government proposes the following:

- The first purchaser of a commercial or industrial property after 1 July 2024 will be able to choose to either pay:

- the property’s final stamp duty liability as an upfront lump sum (currently imposed at top rate of 6.5 per cent), or

- transition to an annual payment immediately by opting to pay fixed instalments over 10 years equal to stamp duty and interest with a government-facilitated transition loan.

- 10 years after the acquisition, the owner of the commercial or industrial property will commence paying the annual property tax which is to be levied on 1 percent of the unimproved value of land.

- Once a property enters the new system after this time, stamp duty will never again be payable on a transaction and the annual property tax will apply.

- The reform will not affect current owners of commercial and industrial properties and will only be subject to the new system once the property transacts after 1 July 2024.

![]() Source: Grant Thornton Australia

Source: Grant Thornton Australia

Click to enlarge

The Government will consult with businesses and industry in the coming months, with legislation expected to be released by the end of the year.

The proposal raises a number of questions which will need to be considered prior to implementation, including:

- Will commercial and industrial properties remain outside the scope of the new property tax indefinitely until sold?

- How will the new property tax interact with landholder duty, in relation to the purchase of shares or units in a trust which owns commercial or industrial property?

- How will commercial and industrial properties be defined and how will mixed use land be treated?

- Will other state property taxes, including land tax and rates continue to be payable?

- What will be the terms of the “government facilitated” loan?

Changes to payroll tax

The Government also announced the following payroll tax changes:

- From 1 July 2024, the tax-free threshold for payroll tax will be increased from $700,000 to $900,000, with a further increase to $1 million from 1 July 2025.

- A ‘phase out’ of the tax-free threshold for some businesses will also come into effect from 1 July 2024. The phase out will result in the tax-free amount reducing for each dollar a business pays in wages over $3 million. Businesses with wages over $5 million will not benefit from the tax-free threshold.

- From 1 July 2024, the payroll tax exemption for high-fee non-government schools will be removed. Approximately 110 schools, or around the top 15 per cent by fee level, will lose their exemption. The Minister for Education will determine, with the consent of the Treasurer, the non-government schools that will continue to be exempt from payroll tax.

As part of a Covid Debt Repayment Plan, the following payroll tax changes will take effect from 1 July 2023 for 10 years, until 30 June 2033.

- An additional payroll tax levy on large businesses with national payrolls above $10 million a year will apply.

- A rate of 0.5 per cent will apply for businesses with national payrolls above $10 million, and businesses with national payrolls above $100 million will pay a levy at a rate of 1%.

The additional rates will be paid on the Victorian share of wages above the relevant threshold.

Payroll tax exemptions, such as those for hospitals, charities, local councils, and wages paid for parental and volunteer leave will continue to apply.

Changes to land tax and land tax absentee owner surcharge

In relation to land tax, a number of changes will take effect from 1 January 2024.

As a part of the Covid Debt Repayment Plan, for a temporary period of 10 years:

- The general tax-free threshold for land tax will decrease from $300,000 to $50,000. There will be no change to the minimum threshold for trust taxpayers.

- For general taxpayers (i.e non trust, non-foreign persons), a temporary fixed charge of $500 will be levied on taxpayers with landholdings between $50,000 and $100,000, and a temporary fixed charge of $975 on taxpayers with landholdings between $100,000 and $300,000.

- For general taxpayers with property landholdings above $300,000 (and trust taxpayers with property holdings above $250,000) land tax rates will temporarily increase by $975 plus 0.1 per cent of the value of their landholdings above $300,000.

- Existing land tax exemptions, including for primary places of residence, primary production land and land used by charities, will continue to apply.

Other non-temporary measures announced to apply from 1 January 2024, include:

- The absentee owner surcharge rate will increase from 2 per cent to 4 per cent.

- The land tax exemption for principal places of residence under construction or renovation will be expanded to provide the Commissioner of State Revenue with discretion to extend period by two years if builder goes into liquidation.

- A new land tax exemption will apply to land owned by an immediate family member and used as the home of an individual eligible to be a beneficiary of a special disability Trust, including where a special disability trust has not been established.

Abolition of business insurance duty

From 1 July 2024, business insurance duties will be progressively abolished (these apply to public and product liability, professional indemnity, employers’ liability, fire and industrial special risks, and marine and aviation insurance).

Abolition will be achieved by 2033, with the rate of duty, currently 10 per cent, being reduced by 1 percentage point each year from 1 July 2024.

Legislation in relation to the above payroll tax, land tax and insurance duty measures is expected to be released shortly.

Grant Thornton will be following the announcements released as part of the State Budget closely over the coming weeks and months. Please contact a member of the Grant Thornton team if you have any queries or would like to discuss.

Victorian State Budget: Driving down the Deficit