The economic health of the retail sector isn’t something that the Government can directly influence. However, it can help to provide the right conditions for consumers to spend and provide incentives for retailers to invest in areas like online and digital.

The data we have from the last 10 years in our ‘Federal Budget: A 10 year retrospective’ demonstrates quite clearly that retailers live or die on their commerciality. In terms of investment, the data we have is from the Department of Industry, Innovation and Science – primarily relating to consumer products rather than retail trade.

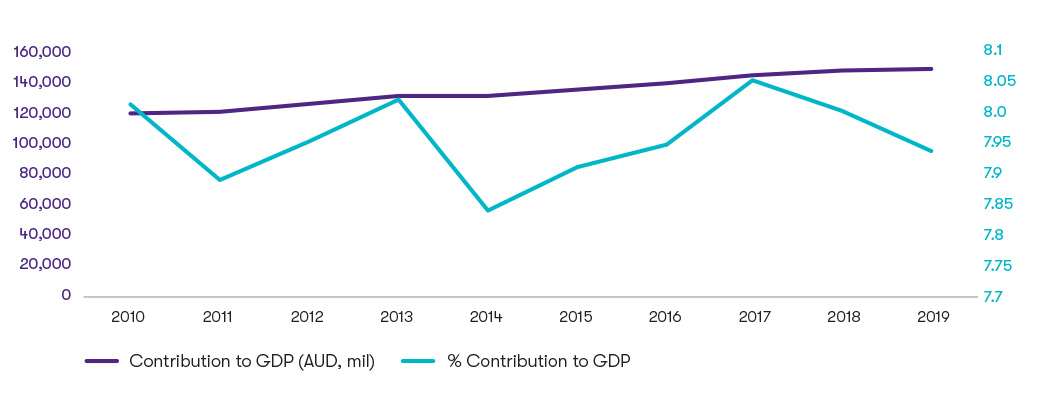

Where the Government has historically intersected with the sector – and will continue to do so – has been around industrial relations, particularly as the sector employs more young people than any other sector, and also has a large proportion of the nation’s part-time and casual workers. In a sector under threat, that is a large number of jobs to be displaced.![GTAL_2020_Retail_FB_Graph.jpg]()

The changing shape of retail

The reality is, COVID-19 has only sped up changes that were already afoot in the industry. What’s happened in the last six months is that there are fewer people in shops, and more people online. But retailers and consumers alike are changing the way they interact and operate. The tenancy mix has changed. We’ve seen a surge to online, and retailers meeting the demand by investing in their online operations.

The Federal Government has done a good job in providing stimulus to both consumers and retail businesses to spend, although the recovery will not be an even one. Some states like Queensland and Western Australia are already performing well, whilst others – notably Victoria – remain in the midst of heavy COVID-19 regulations. But retailers are resilient. Targeted investment in digital and online can be written off the same year under the new guidelines, improving cash flow. Consumers should be buoyed by the extra cash in their pockets and feel confident to spend. Rebuilding consumer confidence will be a long game played by both policymakers and retailers.

In our report we cover:

- An industry left to its own devices

- The great shift online

- Industrial relations

- The role of automation

- Monetary policy and confidence

- So where to from here?

![GTAL_2020_Federal-Budget-2020-21.jpg]()

Looking back to look forward

We were initially writing the ‘Federal Budget: A 10 year retrospective’ report before COVID-19 as an advocacy piece for more industry investment and support. Of course, the way the year started is not the way the year is ending. Many sectors that had been left to their own devices are now key for our recovery. Sovereign capability. Jobs. Digital economy. Modern manufacturing. Renewable future. Deregulation. Innovation. These are the terms we will use as we settle into COVID-normal.

Our report looks retrospectively at 13 different industries, the investment made into them by Government and their contribution to GDP. This is then overlaid with the opportunity we see for industry in this new normal based on recent Government announcements.

Download report