Commencing in 2021, the Federal Government has announced a new, simplified small business restructuring process for small businesses as part of the economic relief reforms.

The Small Business Restructuring Process (“SBRP”) is designed to assist businesses restore operational liquidity by severing the financial burden of legacy debts through a formal debt compromise with creditors.

Unlike other formal restructuring procedures, the SBRP allows for Company Directors to remain in control of and continue to trade their business during the restructuring period.

Qualifying for the SBRP

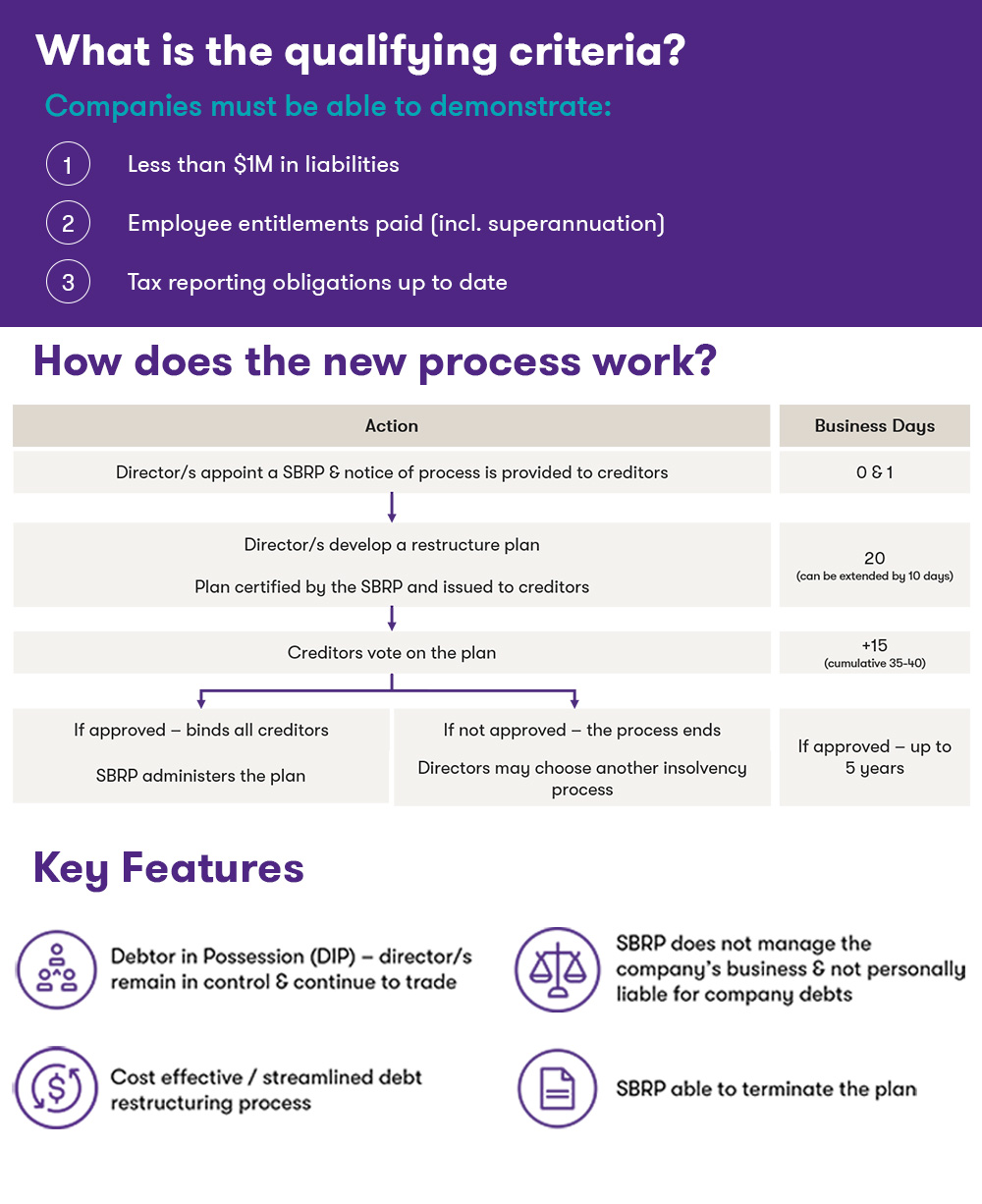

Companies wishing to utilise this process must be able to demonstrate the following:

less than $1 million in liabilities (excluding liabilities to employees of the Company);

all outstanding employee entitlements, including superannuation, must have been paid (nb. this does not include entitlements not yet due for payment, such as annual or long service leave); and

all tax lodgements for the company must be up to date.

Developing a plan: How does the new process work?

On commencement of the engagement of a small business restructuring practitioner (“SBR practitioner”), all unsecured and some secured creditors (eg Retention of Title and Lessors) are prohibited from taking action against the company to recover money and/or collect property (including terminating contracts and formal debt recovery proceedings).

Over the next 20 business days, the Company’s Directors (working with the SBR practitioner) develop a plan to restructure the company’s unsecured creditor debts and collate relevant documents to support the plan, which will ultimately be for creditor consideration. Typically, a plan creates a pool of monies which is applied in full and final settlement of all unsecured creditor debts, excluding related party debt that existed at the time of entering the SBRP. The pool of monies could be funded from various sources, including:

third party contributions

proceeds from the sale of assets

future trading profits

refinance

As a tool to compromise creditor claims, the funding pool does not need to provide for the payment of creditor claims in full. The circumstances of each case will determine the necessary structure and quantum of the funding pool. In almost all cases, the outcome to creditors should be greater than the expected return if the Company were to be placed in Liquidation.

At or before the end of the 20 business days, the SBR practitioner certifies the plan based on their assessment of the Company’s financial affairs and issues the plan to creditors for their consideration.

After receiving the plan, creditors have 15 business days to vote on the plan. If more than 50% in value of unrelated creditors that participate in the vote support the plan, it is approved and binds all unsecured creditors.

If the plan is approved, the business continues to trade under the control of the Directors and the practitioner administers the plan and distributes funds to creditors.

Whilst a rejection of the plan does not necessarily lead to a Liquidation of the Company, the Directors may need to consider the ability to continue trading the Company if it is unable to demonstrate viability.

During the restructuring period, a personal guarantee cannot be enforced against a Director or one of their relatives.

During the restructuring process, the Company’s Directors retain control of the company, which in turn helps to minimise costs and business disruption. We expect that, in most cases, the professional fees for conducting a SBRP will be less than the cost of conducting a more traditional external administration (such as a Voluntary Administration or Liquidation).

The professional fee of the restructuring professional for developing the restructuring plan and liaising with creditors about the SBRP is agreed and fixed up-front.

Our experience is that most SMEs find it difficult, costly and commercially embarrassing to pursue a path of agreeing an informal compromise with creditors.

The ATO is more often than not a significant creditor in corporate insolvencies, however the ATO’s policy on compromising debts (other than penalties and interest) outside of an external administration is quite onerous and difficult to satisfy.

The SBRP provides a simple and cost-effective procedure for companies with unmanageable legacy debts to settle those and other debts, while at all times retaining control of the Company and its business.

A wrap up. What does this mean for key stakeholders?

Advisors to small businesses should be aware that while on its face the SBRP may appear an attractive proposition, failure to properly consider key stakeholder concerns (funding continued supply, lender support and recapitalisation sources) prior to formally entering into a SBRP could result in business failure rather than rescue.

For more information on insolvency reforms to support small business please see:

It is important for business owners facing financial distress to understand all the options available to them. Small Business Restructuring (SBR) offers a pathway for small and medium sized Australian companies experiencing financial pressure to deal with unmanageable debt, reset operations, and continue trading through and beyond difficult times. SBRs are also a cost-effective solution to save a business compared to a liquidation shut down.

As this year’s series kicks off in late 2025, continuing through to June 2026, we will bring you virtual on-demand webinars featuring guest speakers, legal and industry experts, and Grant Thornton specialists sharing insights and expectations for the year ahead.

Subscribe now to be kept up-to-date with timely and relevant insights, unique to the nature of your business, your areas of interest and the industry in which you operate.