In Australia, superannuation serves as a long-term investment for retirement savings and becomes accessible only once specific conditions of release have been met or when an individual has retired.

Total Superannuation Assets on 30 June 2023 were $3.6 trillion and of this, self-managed superannuation funds (SMSF) held $0.9 trillion in total assets. According to the latest SMSF Quarterly Statistical Report, there are more than 600,000 SMSF’s in Australia that represent over 1.1 million members versus APRA regulated entities that make up 22.3 million member accounts and $2.5 trillion of assets

(Annual superannuation bulletin highlights June 2022 – APRA).

SMSF’s can present individuals with opportunities for taking greater control of how their superannuation monies are invested and what they are invested into.

Top three benefits of a SMSF

1. Investment Control

An SMSF offers a range of additional asset classes to invest in such as direct property, gold, collectables, managed portfolios and crypto currency. An SMSF is required to have an investment strategy and the trustees need to think about and articulate how they plan on investing superannuation monies as well as the risks involved.

Consideration into the age group of the members and their risk profiles also play an important role. Liquidity of the fund’s assets, ability to pay member benefits and fund expenses, as well as insurance cover such as life insurance all must be considered.

2. Estate Planning

A SMSF can include up to six members, providing opportunity for the next generation to have their superannuation pooled into the one place. Estate planning within an SMSF is important as it can be the difference between keeping assets inside the SMSF, paying less tax upon death, and ensuring compliance is maintained.

3. Tax effectiveness

The current tax rate on earnings inside Superannuation structures is 15 per cent. When the individual(s) reach retirement and commence a retirement phase income stream, there is no tax payable within the fund on that income. Having the control over the investment decisions allows greater choice on when to dispose assets saving in potential capital gains tax liabilities. Proposed changes to tax on superannuation can be found here.

How should a SMSF be set up?

An SMSF must be set up for the sole purpose of providing retirement benefits to its members.

Setting up an SMSF involves creating a trust with either individual or corporate trustees. Trustees are ultimately responsible to manage the SMSF assets and are responsible for ongoing legal compliance with superannuation and taxation legislation.

An SMSF investment strategy is required, and the trustees need to think about and articulate how they plan on investing superannuation monies. They should consider the risks involved in making certain investment decisions, as well as the composition of the fund’s investments and the extent to which there is a diverse range of assets and asset classes. Consideration into the age group of the members and their risk profiles is also an important factor.

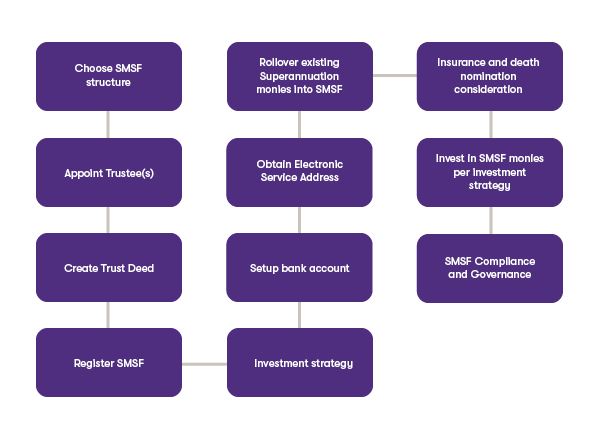

The process

It is critical that your SMSF is set up correctly to receive tax concession and eligible contributions. Remember that if you wish to establish an SMSF you are in charge, so we recommend engaging an expert to help facilitate and provide advice during this process.

The diagram below summarises the process of setting up an SMSF:

![]()

How we can help you

At Grant Thornton, we offer a National Superannuation team to support you and your family with the accumulation phase right through to retirement. For further details, or advice and guidance on the how and why to set up an SMSF, please reach out to your local adviser today.

General Advice

This information is intended to provide general advice only and does not take into account your objectives, financial situation or needs. Before acting on any of the information, you should consider its appropriateness, having regard to your own objectives, financial situation and needs. If you are considering acquiring or continuing to hold a particular financial product, you should obtain the Product Disclosure Statement (PDS) relating to the product and consider this before making any decision. The information in this document been prepared by Grant Thornton Wealth Advisory Services Pty Ltd ABN 61 007 073 305 AFSL 24500.