The first Payment Times Reporting Register was published on 30 November 2021, and covered the reporting period 1 January 2021 to 30 June 2021. The Register – available to download via https://register.paymenttimes.gov.au/ – includes information on the payment times, as well as the Standard Payment Terms (“SPT”), for 6,000+ entities.

Allowing greater access to the payment times performance, as well as the payment terms offered by large businesses in Australia, will enable small businesses to be more discerning as to who they choose to work with, and how long it will take to have their invoices paid.

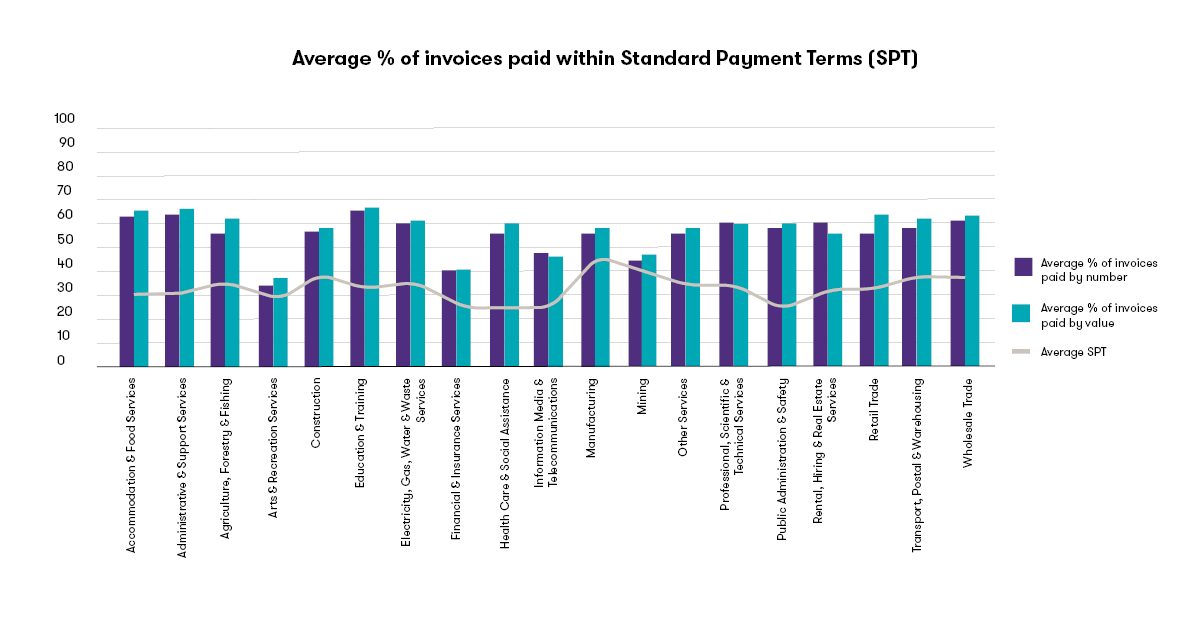

An effective way of interpreting the data contained in the Register is to look at the SPT offered by an entity at the start of the reporting period, and then look to see if the largest proportion of small business invoices are actually paid within that number of days. For example, if an entity has reported their SPT as 30 days, ideally, you would expect the largest proportion of invoices to be paid “Within 20 Days” and “Between 21 and 30 Days”.

![Average % of invoices paid within SPT.png]()

The graph above shows the average SPT at the start of the reporting period for each of the industry divisions. The average SPT is layered on top of the average proportion of small business invoices – by number and by value – reported as being paid within the average SPT. For example, large businesses, which fall within the Education & Training division have an average SPT of approximately 32 days. On average 65% of the total number of small business invoices, and 67% of the total value of small business invoices were paid within 32 days across the Education & Training division.

For small businesses, the Register can provide valuable insight as to what to expect, when considering whether to engage or trade with a large business. It can also act as a strategy tool, to help plan, assess, and calculate the timing of future invoice payments, and cash flows.

For large businesses, if your payment terms are too long or not on par with the average payment terms offered by your industry, the Register can act as a benchmark, and help you to start evaluating what is holding you back from paying small business invoices earlier. Is it your own cash flow concerns? Is it your procurement processes? Or accounts payable processes? Grant Thornton have the people, knowledge and experience to help you improve your payment times performance.

Read the full article here for further analysis on the Payment Times Reporting Register, information regarding the reporting requirements, and the future consequences for non-compliance.

How Grant Thornton can help with Payment Times Reporting

Whilst the second Payment Times Report – due by 31 March 2022 for entities with a standard or calendar income year – is penalty free, we want to ensure all reporting entities fully understand their reporting requirements and obligations. Key questions to start thinking about include:

- Do you meet the eligibility criteria for reporting? If you are a member entity of a group, this is an important point to establish before proceeding any further.

- What do you do if you don’t have SPT, but rather, you pay suppliers according to the terms indicated on the invoice?

- What invoices do you include and exclude from reporting?

- Do you have to report on invoices, which are paid on your behalf by another member entity?

- Who in your organisation can approve the report?

The first reporting period saw a range of challenges and uncertainties from our clients. However through our range of service offerings, tailored to support client needs, we were able to support our clients transition and implement a PTR process that is simple, efficient and hassle-free.

Our support, coaching, and implementation services range from:

- Setting up a framework and processes

- Assessment of systems for PTR suitability, and the data points available

- Assessment of readiness for compliance with PTR requirements

- Building team capacity to comply with obligations, including training

- Testing of reporting outputs for completeness and accuracy

- Ongoing reporting obligation support including lodgement of reporting